How to Improve Your Credit Score (Simple Steps to Save $20,000+)

These simple steps to improve your credit score can save you thousands of dollars over your lifetime.

Consider this from LendingTree:

Borrowers with four common debt types — credit cards, personal loans, auto loans and mortgages — could save $22,263 over the lifetime of the credit and loans by improving their credit score from fair (580 to 669) to very good (740 to 799).

A good credit score isn’t just a number. It’s a key that opens doors to financial freedom.

Want to save this idea?

What Is a Credit Score?

Credit scores represent your creditworthiness. People want to know how safe it is to loan you money.

It’s a number representation of your ability to handle credit. The scores range from 300 to 850.

Higher scores indicate that you’re more “trustworthy” in the eyes of lenders.

Lenders use credit scores to decide whether to approve you for loans and what interest rate you’ll receive.

How do They Decide Your Score?

Scores are calculated using your credit history and behaviors with financial products.

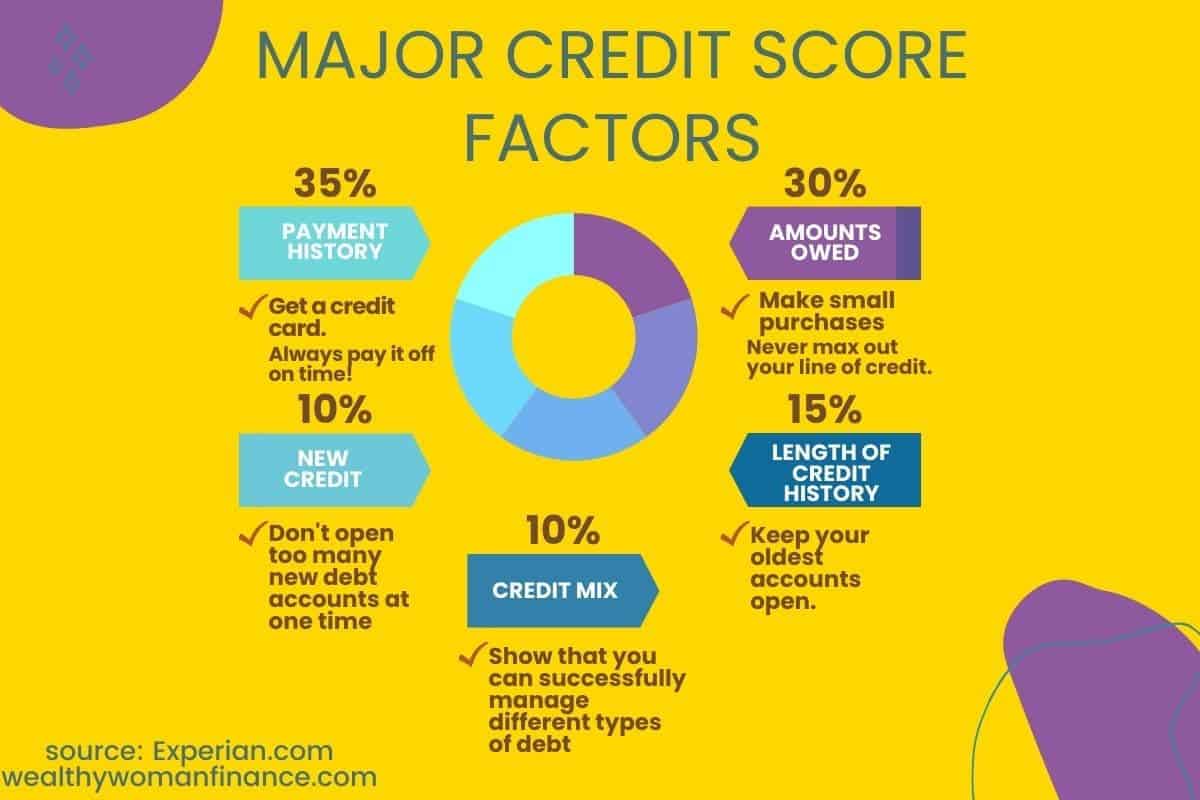

Payment History (35%)

Your payment history is the most significant factor in your credit score. Paying all your bills on time is essential.

Amounts Owed (30%)

This is the ratio of your current credit card balances to your credit limits. Keeping this ratio below 30% can positively affect your score.

Length of Credit History (15%)

The longer you’ve had credit accounts, the better. Lenders favor lengthy credit histories with frequent, responsible use.

When my husband and I first married, he had a better score than I did. Why? Because his parents got him a credit card in high school (only used for gas). This lengthened his credit history significantly.

New Credit Inquiries (10%)

Frequent applications for new credit can lower your score. Each inquiry represents potential risk to lenders.

Credit Mix (10%)

Having a mix of different credit types, like credit cards and installment loans, can boost your score.

Why a Good Credit Score Matters

A good credit score qualifies you for lower interest rates on loans and credit cards. This applies to mortgages, car loans, and personal loans.

Think of it this way: a credit score that saves up to 1% in interest on a mortgage, could mean saving at least $200 per month.

As if saving hundreds or thousands wasn’t enough, here are other reasons your credit score is crucial.

- With high credit, you may enjoy better terms on leases and insurance premiums.

- Some employers check credit scores when making hiring decisions. A solid score can widen your career opportunities.

- Renting an apartment or signing up for utilities often requires a credit check. Higher scores can lead to easier approvals and better conditions.

- You can secure better financing terms for your small business. This helps your business grow and succeed.

How to Find Your Credit Score

You can obtain a free credit report from each of the three major bureaus: Equifax, Experian, and TransUnion, once a year.

Steps to navigate credit reports:

- Access your reports: Use AnnualCreditReport.com to get your free reports.

- Check for errors: Look for inaccuracies such as incorrect personal information or erroneous accounts.

- Dispute inaccuracies: If you find errors, file disputes with both the credit bureau and the creditor.

Regularly reviewing your credit reports helps you spot potential issues early!

How to Improve Your Credit Score

Taking steps to improve your credit score can significantly impact your financial health. These actions collectively improve your score.

Pay Bills on Time

Ensure all bills, including credit cards, loans, and utilities, are paid on or before their due dates to build a positive payment history.

Setting up automatic payments is one effective way to ensure you never miss a due date!

Reduce Credit Card Balances

Aim to keep your credit card balances below 30% of your total credit limit. Paying down high balances can significantly improve your credit score.

For instance, if your credit limit is $5,000, try not to carry balances over $1,500.

Paying down high balances not only helps your credit score, but also reduces the interest you pay over time. Set up automated payments!

Related: Debt Free Payment Trackers

Also, using credit utilization strategies can help. For instance…

- Pay down balances before the billing cycle ends. Or make payments throughout the month to continually keep the balance low.

Avoid New Credit Inquiries

Each hard inquiry can lower your score slightly for a short period. So only apply for new credit when necessary.

Instead, focus on managing the credit you already have. If you need to open new credit, research and plan accordingly.

Check Credit Reports for Errors

Obtain your free credit reports from AnnualCreditReport.com and check for inaccuracies.

It’s recommended to review your credit report at least once a year. Set alerts for any changes to your credit report, which helps keep track of new credit inquiries or potential identity theft.

Increase Credit Limits

If you have a good payment history, request an increase in your credit limits. This can lower your credit utilization ratio.

You can also ask to become an authorized user on a friend or relative’s account (someone who has a good credit score themselves). This person doesn’t even have to let you use the card or account number.

Diversify Your Credit Mix

A mix of credit types, such as credit cards, installment loans, and mortgages, can boost your score. However, avoid taking on debt unnecessarily.

Keep Old Accounts Open

The length of your credit history affects your score. Keep older accounts open and active to show a longer credit history.

Catch Up on Past Due Accounts

Prioritize catching up on payments and consider negotiating with creditors for a payment plan that works for you. Good communication can alter the terms of your agreement (in your favor) to ensure they receive their money. A win-win for both of you!

Steps for negotiation:

- Gather information: Know your account details and payment history.

- Contact the creditor: Call your creditor to discuss your situation.

- Propose a plan: Suggest a revised payment plan or settlement amount.

Often, creditors will consider reducing your interest rate or monthly payment if they see you are making a genuine effort to pay.

Some creditors may even agree to report your account as current after a series of on-time payments.

Ask for late payment forgiveness

If paying late is a one-time offense, call the company and ask them to forgive your late payment. In most cases, they will!

Use a Secured Credit Card

This type of credit card requires a cash deposit as collateral.

Building a Strong Financial Future

A healthy credit score is vital when making big purchases like buying a home or buying a car.

A higher score can save you considerable money over the life of a loan. So, when you’re planning for your financial future, don’t forget about the incredible power of your credit score!

What’s Next?

Grab ongoing wealthy woman ideas in the newsletter. Make money-smart decisions your default, plus gain instant access to the free resource library.