4 Free Debt Tracker Worksheets: Crush Debt in 2026

Are you swimming in debt? Whether it’s a baby pool or an ocean, you CAN get out of it.

What matters is that you are here and willing to put in the work. Kudos to you!

Now, let’s get to a few numbers and get those free debt tracker printable charts rolling.

How much debt does an average person have?

First, if you are struggling with debt, you are not alone. Take a look at the average U.S. amounts for 2021.

| Loan Type | 2021 Average Amount | |

| Credit Card & Personal Loans | $22,285 | |

| Auto Loan | $20,987 | |

| Student Loan | $39,487 | |

| Home Equity & Mortgage Loans | $259,936 |

Want to save this idea?

Unless it’s a strategic investment, the debt you carry is stealing from your future self. You have to pay thousands of dollars extra in interest for your stuff, cars, education, and more. Let’s end the madness and give you the gift of financial freedom instead.

How do you create a debt free plan?

Ok, you are ready to roll. But how do you create a diy debt management plan?

Here’s how to set up your debt payment plan:

1. Run the numbers

First, find out exactly how much debt you have. Write down the type of loan (i.e. medical), the name of the lender, the amount owed, the interest rate, and the minimum due each month.

2. Decide which method you will use to pay it down

A question that’s often asked is “what is the most highly recommended method of paying off debt?” There are two popular methods:

Debt Snowball Method

With the debt snowball approach, you

- Prioritize debts from smallest in size to largest

- pay off your smallest debt first (while making minimum payments on the others)

- repeat until all debts are paid off.

This method is meant to help you build momentum because you will knock off individual debts faster. (It is like a snowball rolling down a hill, picking up steam and continually getting bigger.)

Debt Avalanche Method

With the debt avalanche approach, you

- prioritize debts from highest interest rate to lowest

- pay off your highest-interest debt first (while making minimum payments on the others)

- repeat until all debts are paid off.

This method saves you more money because you are chopping off your high-interest rates. It may take you longer to pay off an individual debt (so you’ll need to stick it out when the going gets tough), but you keep more cash in your pocket.

Which is better?

In the end, as long as you use one of them or a hybrid approach, you’ll have the same result ~BEING DEBT FREE.

It’s the consistency that matters.

3. prioritize your debts & Start A Plan

Which debt will you pay extra on first? Which one will be next?

And which ones will you pay only the minimum? Prioritize your debts in number order.

4. Look at Your Budget To Lower Expenses

Next, look at what you have been spending over the last three months. Where can you cut back?

Check out these creative ways to save and cheap things to do on a budget to help you brainstorm less expensive ways to spend your time.

5. Target The High Impact Expenses to Save Big

Your Top 3: People spend the majority of their money on housing, cars, and food. One key financial decision with these can save you the MOST money over time. A cheaper house or car can be the only move you need to crawl out of debt for good.

That’s working smarter. Not harder.

Your recurring expenses: Tv streaming services, memberships you don’t use, and app subscriptions are small but add up over time.

Also, think about how you can lower insurance and regular bills. Sometimes, one phone call or a quick shop around can save you big.

6. Hit Your Debt From All Sides

Next, lowering your expenses allows for easy wins. But there are other ways to pulverize your debt too. Here are a few.

Make More Money

Sometimes it isn’t that you do not save money. It’s that there’s not enough coming in. Consider a side hustle, find ways to make an extra $500, switch jobs, negotiate your salary, or build passive income streams to accelerate your progress.

Negotiate Or change The Loan

Making several calls to creditors can help you lower interest rates or change the payment dates. Similarly, refinancing mortgage loans can help with this as well.

Make Doing the Right Thing EASY

Building better money habits is all about making the “right thing” the path of least resistance.

- Set your larger debt payment on auto-pay.

- Freeze your credit cards and use an envelope system to keep track of your money until you get your big debts paid off.

- Put your free debt tracker where you walk by often.

- If you keep track of spending online, bookmark your financial software site or keep your spending charts on your computer desktop.

How can I motivate myself to pay off debt?

Staying motivated and on track is the BIGGEST challenge when paying off debt. Try one (or ALL) of these on your way to financial success.

1. Consistently use the free debt tracker printables below. The visual progress will keep you going!

2. Pay off debt with a friend or family member. Or join an online group that is sharing success stories. Community is a powerful motivator!

3. Post debt free living quotes up around your home.

4. Shift your mindset with wealth and success affirmations. Change your computer passwords and phone reminders to reflect your new thinking.

5. Write your financial goals daily In fact, studies show that when you write your goals you are 42% more likely to achieve them (source). Better yet, set up a commitment contract.

6. Immerse yourself in financial learning. The more motivational input you can receive through books, articles, and podcasts the better.

7. Monitor your credit and balances so that you can see the impact your payoff efforts make.

8. Treat yourself on a budget when you hit milestones. Did you just pay off $1,000 in debt? Celebrate with a night off of responsibilities.

9. Make a vision board that includes all of your big financial dreams. Seeing a beautiful bright future every time you walk by your desk helps you resist daily temptations.

10. Make saving fun! Join a money saving challenge, turn thrift store shopping into a game, review your spending while you watch your favorite shows, and look for other small ways to enjoy the process.

Related: Best Money Saving Games For Adults

How do you use debt free Pdf charts?

Now, here are all four debt payment trackers depending on which debt you are targeting. Decide on how much money goes towards each. Then, color in the visuals as you go. Have written AND visual progress will help you stay motivated!

Free Credit Card Debt Payoff Tracker Printable

Find more tips to pay off credit card debt quickly >>

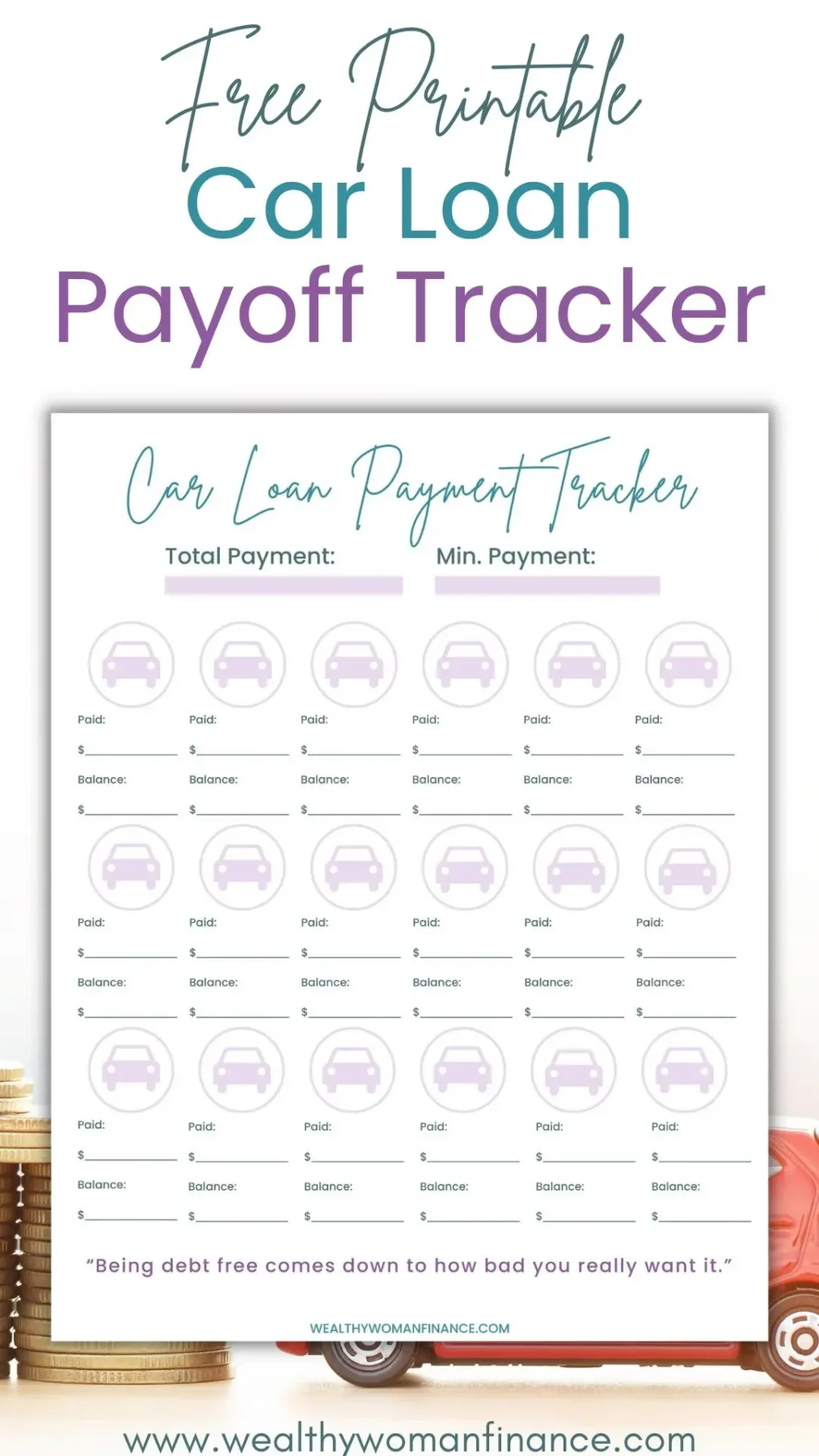

Free Auto Debt Tracker Pdf Template

Free Debt Tracker Worksheet for Student Loans

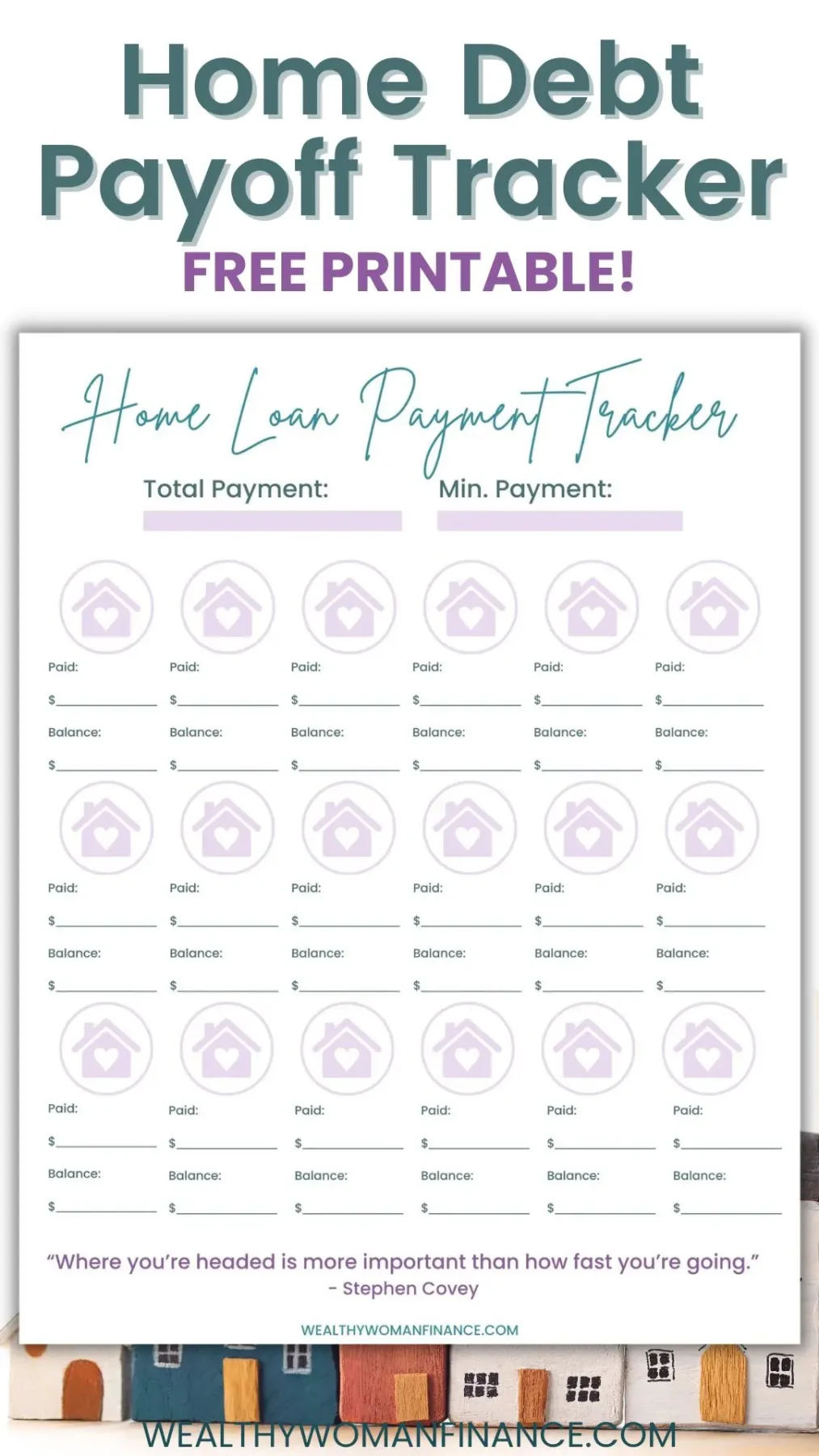

Debt Payment Tracker Printable For Mortgage

Want to save these trackers? Enter your email and I’ll send the link straight to you.

Related: 12 Doable Steps to Pay off Debt Quickly

More Common Q & As: Debt Tracker Printable

How long will it take me to get out of debt?

That, my friend, depends on how laser-like you want to make your focus. And how consistently you pay off debt along the way.

What should you NOT do when paying off debt?

DON’T:

- Go without a plan.

- Try to pay off three debts at once. (Start with one. Focus is key!)

- Neglect to track your progress. Seeing your forward movement is ESSENTIAL to keeping the momentum going.

- Leave no money in your savings account. An emergency fund protects you from further debt.

- Go off the rails. (Read below). Remember the turtle and the hare? The turtle won. Start with doable habits and build over time instead of going crazy and losing steam three weeks from now.

Is it better to pay off debt all at once or slowly?

The more money you can put in sooner the better, as it will save you in interest payments in the long run.

However, if it will take you time to pay off your debt, it is a great idea to integrate your accelerated payments into a slow and steady structure.

Is it better to have money in the bank or pay off debt?

I recommend having enough to cover your basic emergencies first. This will ensure that you don’t have to go into further debt if a minor emergency hits your family.

After that, it is better to pay off debt because that money is currently going up in smoke.

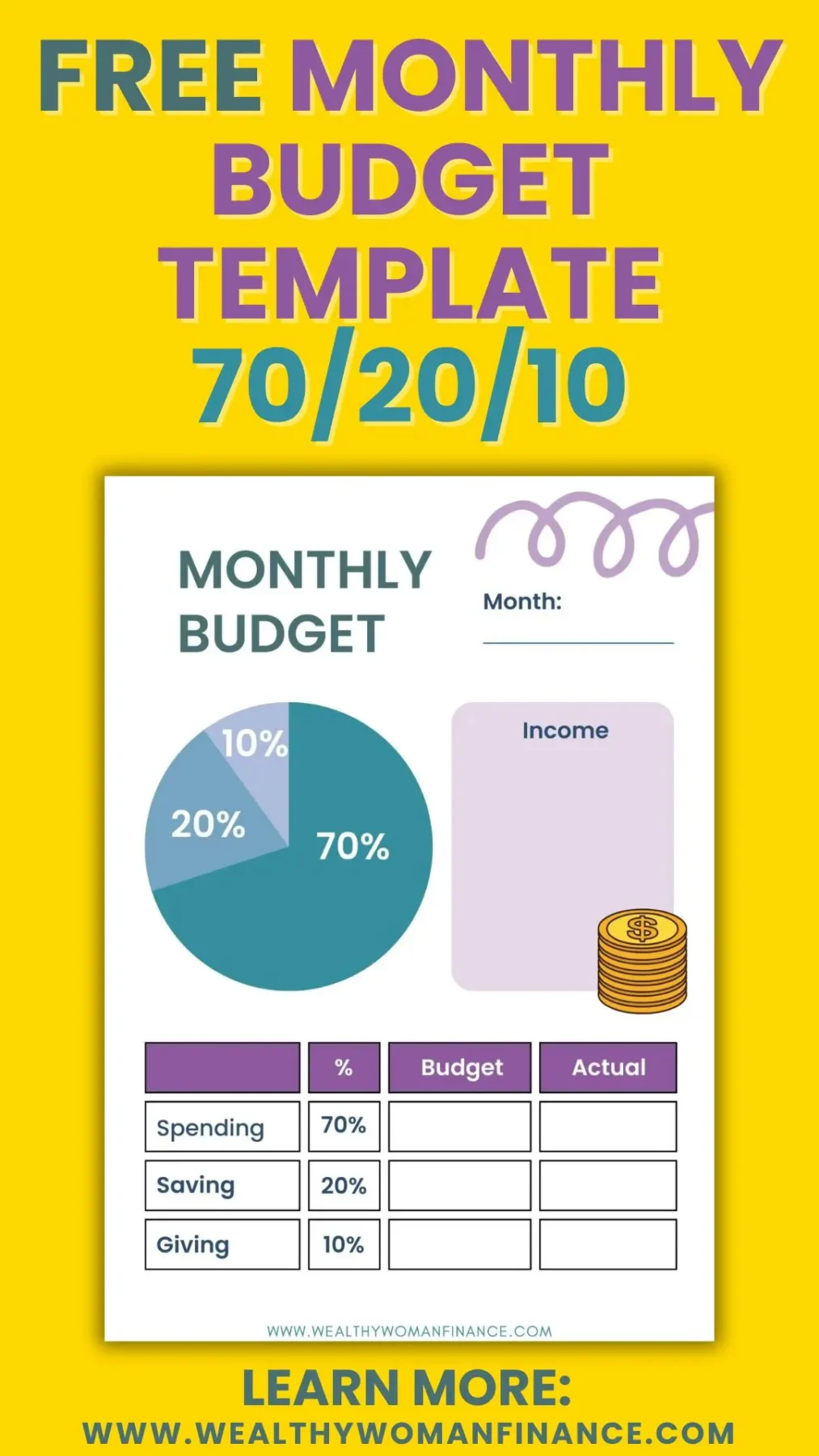

Budget Plans to Help You

Check out these budget plans to help you with paying off debt:

To Consider With Debt Free Tracker Charts

I hope you love them! Leave a comment below to tell us about your progress!