14 Common Money Mistakes That May Be Costing You thousands

Managing your finances can be tricky. Small money mistakes add up over time.

Plus, often you don’t know what you don’t know.

Most people don’t realize how much is slipping through the cracks! And how ignoring the basics can lead to big losses.

But don’t worry. I’ve got your back. Today, explore the common mistakes people make with their money and the fixes you need to address them. Knowing these pitfalls can be a game-changer!

Want to save this idea?

1. Ignoring the Basics

Not tracking your spending might cost you hundreds or even thousands a year. Money disappears quickly when you don’t pay attention. Something as simple as daily coffee or lunch out can add up fast without you realizing it.

Action Step: Try a budget app or keep a small notebook to jot down your expenses. Review them weekly. This small step can show you where money leaks happen, so you can curb your spending.

2. Letting Subscriptions Drain Your Wallet

Then, once a month…

Check your expenses for recurring charges. Things like:

- streaming services

- gym memberships

- digital apps

- and meal kits

Often, you forget about services you no longer use. Yet they still take money from your account each month.

Action Step: Cancel what you aren’t using! Then set a recurring reminder to check your subscriptions monthly or quarterly.

3. Not Realizing that Cash Is Still King

Having quick access to cash is critical. When emergencies come up, like car repairs or medical bills, you need cash fast. Without it, you might have to use credit cards or loans.

It’s recommended to have three to six months of living expenses saved. If you don’t have that, start with smaller goals, like building up $500 to $1,000. This can cover smaller surprises and prevent dipping into debt as you build more.

Action Step: Try the emergency savings challenge to keep you motivated to save!

4. Falling Into Bad Debt

High-interest debts quickly spiral out of control. And it often starts innocently…

Credit Card Prison

Credit cards can be useful. And you should take advantage of credit card rewards if you can.

But if you aren’t paying your card in full each month, the interest adds up fast. The extra you’ll pay far outweighs the benefits.

Action Step: Track your spending so you know how much is too much to put on your card. And if you ever have doubts about whether you can afford something, you probably can’t.

Payday Loans Prey on the Poor

Payday loans are usually short-term, but they often have high fees. These loans can be tempting because they’re easy to get, especially when you’re in a pinch.

The problem is that the fees and interest rates can be extremely high. Borrowing $500 might cost you hundreds in fees if you can’t pay it back quickly.

Action Step: Avoid payday loans to save a lot of stress and money. Use better methods to find emergency cash fast.

5. Not Having Clear Financial Goals

Having clear financial goals helps you spend smartly and invest wisely. Without goals, you save and invest without direction (or motivation). And in this case, your money may not grow as it could.

Tips for Goal Setting:

- Identify Goals: Decide what you are saving for. Is it a vacation, a new car, or retirement?

- Set a Timeline: Know when you want to achieve these goals.

Goals are a tool that help you reach your dreams. They keep your hard-earned money working effectively and reduce stress.

Action Step: Write 3 financial goals you are working toward. Now, what’s your plan to get there?

6. Trying to Time the Market

Likely, you know at least one person who has tried to time the stock market. They want to buy low and sell high. There’s only one problem. Almost no one can accurately predict what the market is going to do. And that includes Harvard MBA grads and so called “experts.”

Aside from setting yourself up for poor timing or sitting on the sidelines, jumping in and out of investments can lead to higher taxes too.

Action Step: Instead, consider long-term investing. Stay calm during market swings. Focus on a well-thought-out strategy that isn’t dependent on what happens in the market today.

7. Putting All Your Eggs in One Basket

Putting all your money in one type of investment is risky. If that investment does poorly, you could lose a lot. This is why diversification is important. It means spreading your investments across different asset types like stocks, bonds, or real estate.

Diversification can lower risk because if one investment drops, others may go up. Think of it as not putting all your eggs in one basket. It helps balance out the ups and downs.

Action Step: You can diversify by investing in a mix of industries or using mutual funds and ETFs. This strategy potentially steadies your returns.

8. Having Too Much Or Not Enough Insurance

Health insurance is crucial because medical costs can be unpredictable and high. Unexpected surgeries, hospital stays, or medications add up quickly. Without coverage, you might face hefty out-of-pocket expenses.

Action Step: Consider plans covering essential services, medications, and specialist visits. Assess your health needs and ensure your plan addresses them. A good health insurance policy can be your safety net in a medical emergency.

After you’ve assessed health insurance, take steps to understand the others as well – renter’s insurance, home insurance, auto, and more. Think through what is enough (but not excessive) for what you need.

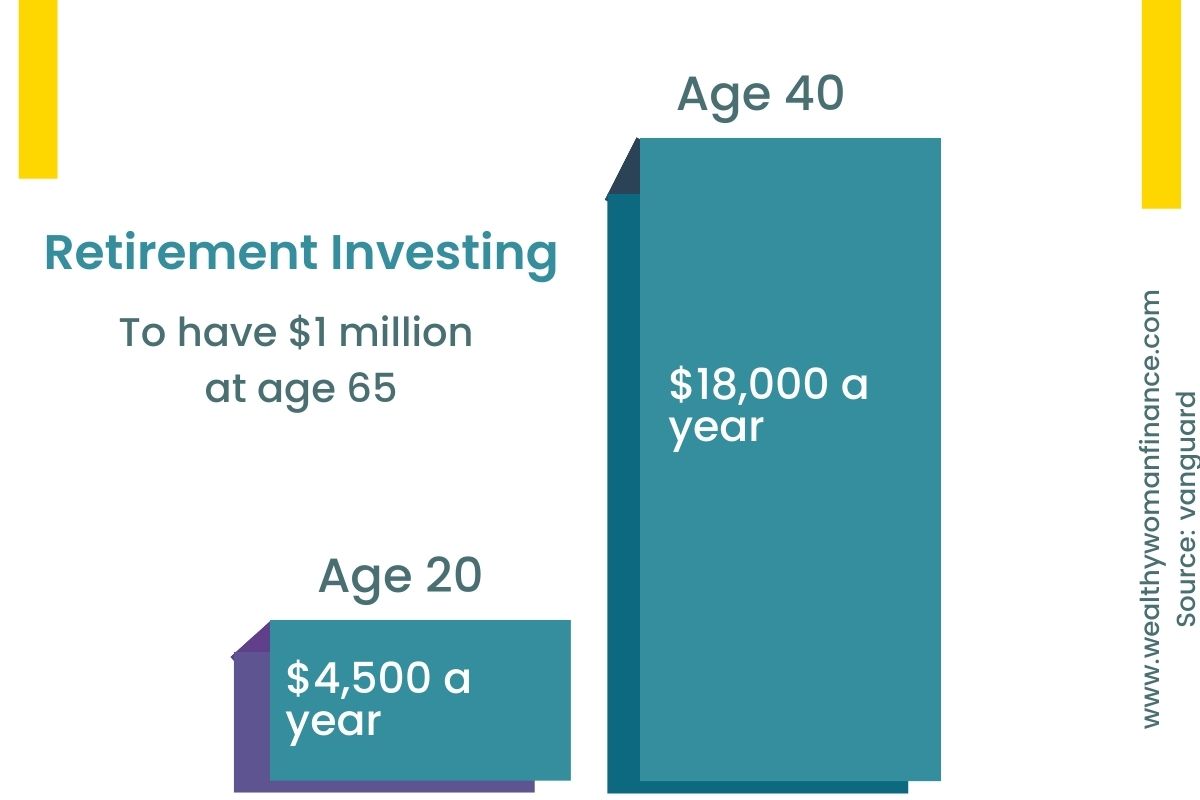

9. Putting Off Saving for Retirement

Delaying your retirement savings can be costly! Don’t miss out on the power of compound interest!

Action Step: Increase your saving and investing by at least 1% today.

10. Not Maximizing Employer Match

When your employer offers a retirement plan with matching contributions, it’s a golden opportunity.

For example, if you put in 3% of your salary, they may add another 3%.

Failing to take advantage of this match is like leaving free money on the table. Think of this match as an instant return on your investment.

Action Step: Contribute at least enough to get the full employer match. Not only does this boost your savings, but it also helps compound interest work in your favor.

11. Ignoring Tax-Advantaged Accounts

Tax-advantaged accounts like 401(k)s or IRAs can be a key part of your savings strategy. Contributions may be tax-deductible or tax-deferred, meaning you could

- lower your tax bill now

- or pay taxes when you withdraw in retirement (when your tax rate might be lower)

Using these accounts wisely can help your savings grow faster. Since you aren’t paying taxes on your earnings each year, you can reinvest the savings and potentially earn more.

If you ignore these accounts, you miss out on these benefits!

Action Step: It’s worth checking the different types available (there are also tax-advantaged health savings and education plans) and consider how they fit into your financial plan. Make saving smarter, not harder!

12. Letting Lifestyle Creep Take Over

Lifestyle inflation quietly eats away at your finances because it’s easy not to notice. (Especially when everyone around you does it)

When you get a raise or a financial windfall, it’s tempting to upgrade your lifestyle. You might think it’s time for a bigger house, a fancy car, or lavish vacations.

These upgrades feel deserved but can cause trouble. If new expenses match income, saving becomes difficult. You end up not having enough, even though you make more money.

Action Step: Prioritize saving a portion of any income increase. And consult your budget before big buys. Remember that keeping your lifestyle simple can create more financial freedom and less stress, at any income level.

13. Compulsive Buying Disorder

Compulsive buying is more than just frequent shopping for fun. It can become a cycle where emotional needs drive you to spend. You chase the temporary joy each purchase brings.

Often, these urges can result in debt or regret.

Action Step: If you often feel an uncontrollable desire to shop, become more aware of your triggers. Consider seeking help or using techniques like mindfulness to control these urges.

14. Falling for Financial Scams

Sometimes, falling for financial scams can be easier than you think. Be wary of schemes that promise quick returns and attempts to steal your personal information.

Pyramid Schemes

Pyramid schemes often promise you wealth if you recruit others into the system. You might see it as an investment opportunity with big rewards.

Action Step: Always ask questions and do your research. Watch out for any plan where earnings primarily depend on bringing in new participants. This is often a sign of a pyramid scheme when victims end up losing their money while the scheme leaders profit.

Phishing Attempts

Phishing scams aim to steal personal information like passwords and credit card numbers. You may receive emails or messages that look genuine, but they are fake. These messages often create a sense of urgency to make you act quickly.

Action Step: Protect your information by using caution when clicking on links or opening attachments. And use security measures like two-factor authentication.

Pro Tip: Look out for poor grammar and misspelled words in emails. These are common signs of phishing.

What’s Next?

Be patient with yourself. Everyone makes mistakes, but by learning from them, you can make better choices in the future. And this is where real wealth is built.

Focus on small steps every day that lead to big improvements over time. You’ll be there before you know it!

Next, learn more! Become a part of the Wealthy Woman community, receive my best tips for wealth-building, and have instant access to the free resource library. Start now!