10 Ways People Go Broke Even on a High Income

Earning a high salary doesn’t guarantee financial security. Many people find themselves struggling despite making a lot of money.

In fact, as of 2024, more than one-third of those earning more than $200,000 a year live paycheck to paycheck (source). They’re broke.

But how can this be?

Want to save this idea?

High Income vs. Wealth: What’s the Difference?

It’s easy to confuse high income with wealth.

Earning a high salary can help. It’s great if you earn a lot from your job or business. This provides the means to build wealth. But it doesn’t automatically make you wealthy.

Wealth, on the other hand, is not just about how much you earn, but how well you manage your money. Are you building your savings, investments, property, and other assets so that they grow over time?

This is your net worth (the value of your assets minus your liabilities).

Consider this: You can earn a substantial salary but have little to no wealth. Contrast this with someone who earns less but saves and invests wisely, steadily building their wealth.

Key Differences

| High Income | Wealth |

|---|---|

| Salary, bonuses, business income | Savings, investments, property, assets |

| Based on earnings from work | Accumulated over time |

| Can be spent quickly | Can grow and provide financial security |

When you focus on building wealth rather than just earning a high salary, you’re working towards long-term financial stability.

Common Pitfalls to Avoid

High-income earners often face financial pitfalls that can lead to big money troubles. In fact, you probably know someone who has fallen into one of these traps!

1. The #1 Trickster

Lifestyle inflation is one of the sneakiest and most dangerous pitfalls. It slowly creeps up over time. This occurs when your spending increases as your income rises. And it’s why so many high earners still live paycheck to paycheck.

Your Habits Get More Expensive

When you start earning more, it can be tempting to adopt new daily routines. You might find yourself going to Starbucks for your morning coffee instead of making it at home.

Or…

- Dining out more often at upscale restaurants instead of having homemade meals

- Signing up for subscriptions or club memberships

- Putting your kids in more and more expensive activities

- Spending more on vices like gambling and alcohol than you used to

Spiraling into these daily habits can make saving difficult, even with a high salary.

Your Lifestyle Gets More Luxurious

Moving to nicer living spaces, buying designer clothes, taking upscale vacations, and driving fancier cars are other ways that lifestyle inflation can get you.

While it might seem justified, these choices lead to less and less in savings.

You work hard and it’s vital to spend your money on what’s most important to you. But be sure to keep your overall expenses in check so that your lifestyle doesn’t eat away at your financial future.

2. Poor Budgeting

Many high-earners struggle with maintaining a budget. And unfortunately, the absence of a clear financial plan often results in excessive spending.

How can you know if you’re overspending if you don’t know what that looks like for you?

A budget is a plan that tracks income and expenses. It ensures you live within your means. It also helps you understand what your true needs vs wants are so that you can make informed choices.

Try the zero-based budget or a percentage-based budget like the 50 30 20 to help you find the right balance for you.

3. Carrying Excessive Debt

High earners still get trapped by debt. (In fact, high earners can be targeted even more by loan officers.)

Credit card balances, car loans, student loans, and personal loans add up. Plus, high-interest rates can make these debts grow faster than expected.

It’s important to manage and pay off your debts as quickly as possible. Build a repayment plan into your budget and stick to it.

Plus, avoid taking on new debt whenever possible. Managing debt effectively ensures your high salary works for you, not against you.

Related: Free Debt Repayment Trackers

4. Not Having Enough in Savings

An emergency fund acts as a financial shield. It is crucial for covering unexpected expenses like car repairs or job loss.

Without this fund, you might end up relying on high-interest credit cards or loans, and accumulating debt on accident.

Financial experts often recommend saving 3 to 6 months’ worth of living expenses. Set up automatic transfers to a savings account to help build a financial cushion. Aim to save at least 20% of your income for emergencies, major purchases, and long-term goals.

Building this fund requires discipline and consistency. But think of how much better you’ll sleep at night having that cushion.

5. Making poor investment choices

Investing is crucial for growing wealth. But poor choices can result in large losses. High earners may fall victim to risky investments, such as high-fee mutual funds or speculative stocks.

My uncle once invested thousands into something from his son-in-law that he admitted to not fully understanding. HELLO red flag!

Keep this from happening!

- Educate yourself about investment options and risks.

- Avoid putting all your capital into high-risk investments

- Balance your portfolio with a mix of stocks, bonds, and other assets to protect against substantial losses.

Consider speaking with a financial advisor to help you make informed decisions that align with your risk tolerance and goals.

6. High Housing Costs

Overspending on rent or mortgage payments is one of the most common mistakes keeping high-income earners broke.

I’ll never forget the first time my husband and I bought a home. It was 2009. The real estate agent looked us both in the eyes and asked solemnly whether we could truly afford the home we wanted to buy. It’s not because he didn’t trust us. At that time, our only buying options were foreclosures. He had seen too many people overextend and lose everything.

When you earn a high salary, it’s tempting to buy a large, expensive home. However, a high mortgage can drain your finances faster than anything else. Being house-poor isn’t worth it!

And your housing expenses include more than just the loan—taxes, insurance, furnishings, utilities, and maintenance are all more expensive too.

7. Supporting Costly Family Members

Providing financial support to family members is commendable but can also strain you. Whether it’s helping parents, siblings, or children, these expenses add up quickly.

So, set clear boundaries and have open discussions with family members to manage expectations. When it comes to things like college expenses, medical bills, and living expenses, make sure everyone is on the same page.

And ensure that you aren’t helping others so much that you are hurting yourself in the process.

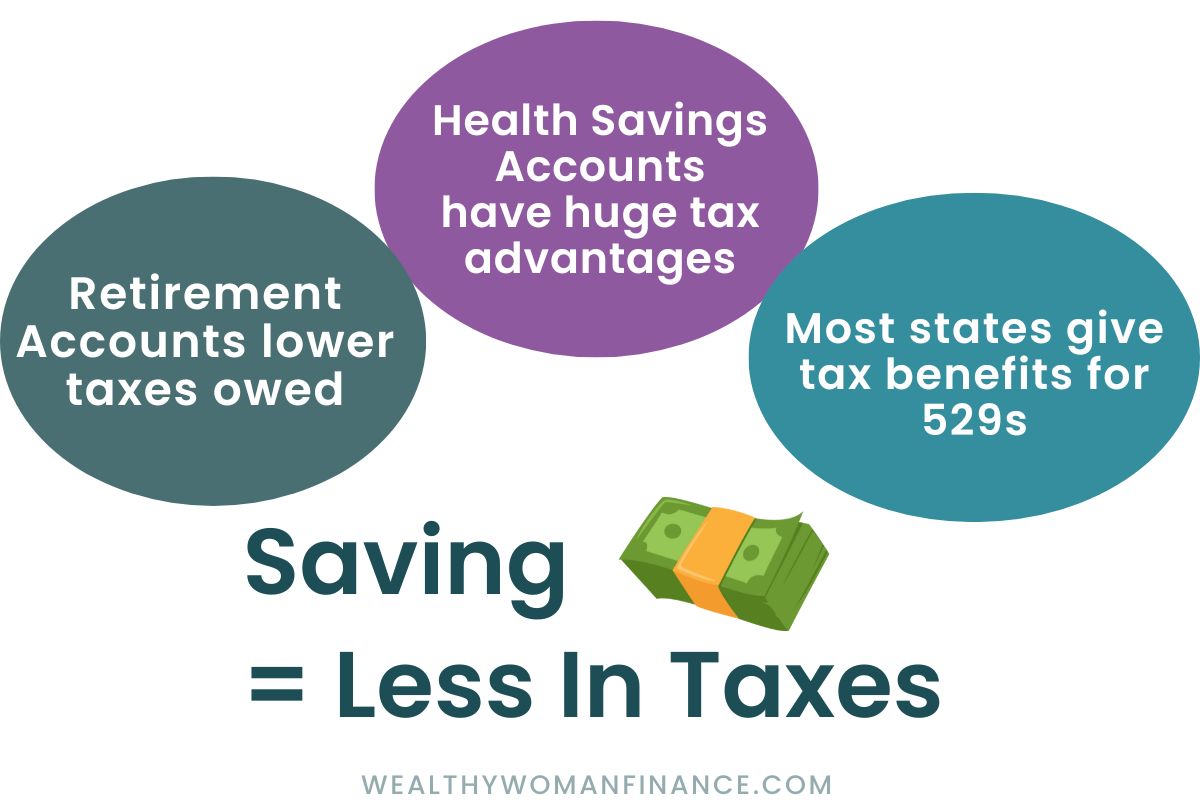

8. Not Planning for Taxes

High earners often encounter higher tax brackets. Failing to account for this can leave you scrambling when tax season rolls around.

Plus, not having a proper tax strategy can result in paying more taxes than necessary.

Planning for taxes throughout the year, rather than waiting until filing season, enables you to make strategic decisions that reduce how much you have to pay.

Consider activities that may reduce your tax bill:

- Investing in Tax-Advantaged Accounts (401K, IRAs, HSAs, 529s)

- Making charitable donations

- Itemizing deductions

- Timing income and expenses

- Claiming all deductions and credits

- Starting a business

9. Neglecting Your Future

This pitfall is far too common in our instant gratification society. It has become commonplace to only look to the next day or week. But an ounce of prevention today (in all areas of your life) can prove to be a pound of cure in your future.

Here are just a few examples:

- Failing to contribute consistently to retirement accounts = missing out on compound interest (tens of thousands of dollars)

- Not taking care of your health = costly medical bills

- Not investing in your marriage = costly divorce expenses

- Ignoring professional development = your earnings can plateau for years

When in doubt, think ahead at least 10 years. How do you want every aspect of your life to look then? What do you need to do NOW to make it that way?

10. Not Protecting Yourself With Insurance

Many high earners neglect essential insurance policies. This leaves them vulnerable to financial burdens in case of unexpected events.

| Without health insurance | medical emergencies lead to overwhelming bills |

| Life insurance | provides security for your loved ones, ensuring they are not financially strained in your absence. |

| Disability insurance | ensures that if you are unable to work due to illness or injury, your income is replaced, preventing a drop in your living standards. |

| Home and car insurance | makes sure that you aren’t overwhelmed by bills in the case of an accident or outside circumstance. |

Having sufficient coverage in these areas can prevent major financial setbacks!

3 Behavioral Pitfalls & How to Counteract Them

You may KNOW what to do, but have a hard time putting it into action. So, next, these negative behavioral factors often deplete your savings. Become aware of them. Then start fixing them so that you can easily put each of the steps above into action.

Impulsive Spending

Impulsive spending, also known as emotional or compulsive buying, is a major problem for many. This behavior stems from a desire to feel good in the moment.

Compulsive spending often happens when you are stressed, anxious, or trying to cope with negative emotions. Retail therapy might provide a temporary boost in mood, but it can severely harm your long-term financial health.

High earners are not immune to this. Access to more disposable income can sometimes make it worse.

Monitoring your habits and emotional triggers can help.

- Create a budget and stick to it. Try cash envelopes if it helps to have tangible money.

- Remove any shopping apps, emails, and other temptations from your devices

- When you start to feel stressed or anxious, find a healthier way to cope, like taking a nature walk or a bath.

Dangerous Denial

Financial denial occurs when you ignore or downplay your financial difficulties. This stems from fear, embarrassment, or a lack of knowledge about finances.

I like to call it “putting your head in the sand.”

But denying financial problems can cause you to make your situation far worse.

Have you ever done this?

- delayed checking your bank statements

- failed to open bills

- underestimated how much you owe

This avoidance can increase debt, deplete savings, and destroy your credit score.

To counteract financial denial, face your finances head-on. Make a recurring meeting with yourself (or an accountability partner) to review your financial status and set realistic financial goals. Transparency and awareness are key!

Not Educating Yourself

Relying solely on personal judgment is risky. Financial professionals and education provide critical insights into savings, investments, and retirement planning. Disregarding this can lead to missed opportunities and getting caught in traps you didn’t know were there.

Accurate financial advice ensures that your high salary translates into long-term wealth. So, seek out financial experts and do your research, especially when making big financial decisions.

Related: 10 Things Money Savvy Women Never Do

What’s Next?

Next, learn more! Become a part of the Wealthy Woman community, receive my best tips for wealth-building, and have instant access to the free resource library. Start now!