7 Ways to Escape the Paycheck to Paycheck Trap

Living paycheck to paycheck can be incredibly stressful. It makes it difficult to enjoy life and plan for your future. If you’re living this way, take control of your finances and break free from the cycle.

Financial security is achievable, and maybe faster than you think!

What is the Trap?

The paycheck to paycheck trap occurs when your income barely covers your immediate expenses. This leaves little to no room for savings or unexpected costs.

Want to save this idea?

According to a 2022 LendingClub report, 64% of the U.S. population lives this way. And it doesn’t necessarily matter what you make either. As of 2024, more than one-third of those annually earning more than $200,000 say they live paycheck to paycheck (source).

Living this cycle results in high stress and anxiety. There’s a constant underlying fear of not having enough money. But it also means you miss out on vital investment opportunities, job changes, and creating your dream life.

As long as you’re in the paycheck-to-paycheck trap, you’ll be running on the hamster wheel. Breaking out of that cage is how you build a life on your terms. Start now!

7 Key Financial Habits to Break the Cycle

1. Create a Detailed Budget

To break free, start by tracking your spending. You need to know exactly where your money goes.

Best Tips For Tracking Your Expenses

- Record every single expense. It’s too easy to let small expenses slide. And this eventually leads to thousands of dollars.

- Categorize your expenses into needs vs wants to get a better big-picture view.

- Use an app or a spreadsheet to log these transactions daily. Regular tracking helps you identify patterns and areas where you can cut back.

- Set a non-negotiable “budget date” weekly or monthly to analyze your expenses.

- Build the habit of expense tracking by making it visual (see the image above – add one to a jar each day). And give yourself small, motivating rewards along the way.

- Take note of irregular expenses such as annual subscriptions, holiday gifts, and car registration fees. These should be averaged out over the year and included in your monthly budget.

Prioritize Your Spending

Once you have a clear view of where your money is going, it’s time to prioritize.

1. Essential expenses like housing, utilities, and groceries come first.

2. After covering your needs, set aside money for savings and an emergency fund. Even if money is tight, aim to save at least $1 per week to build a habit.

3. Once basic needs and savings are addressed, allocate money for your wants, such as dining out and entertainment. Be mindful of your limits to avoid overspending.

Related Budget Plans:

Re-evaluate and adjust your spending priorities as you go. Regularly refining your budget ensures it stays aligned with your financial goals.

Pro Tip: Get as clear on your goals as you can. Make plans. Write out deadlines. Make a vision board. Whatever lights your fire. Motivation comes from knowing EXACTLY what you want and reaching for it.

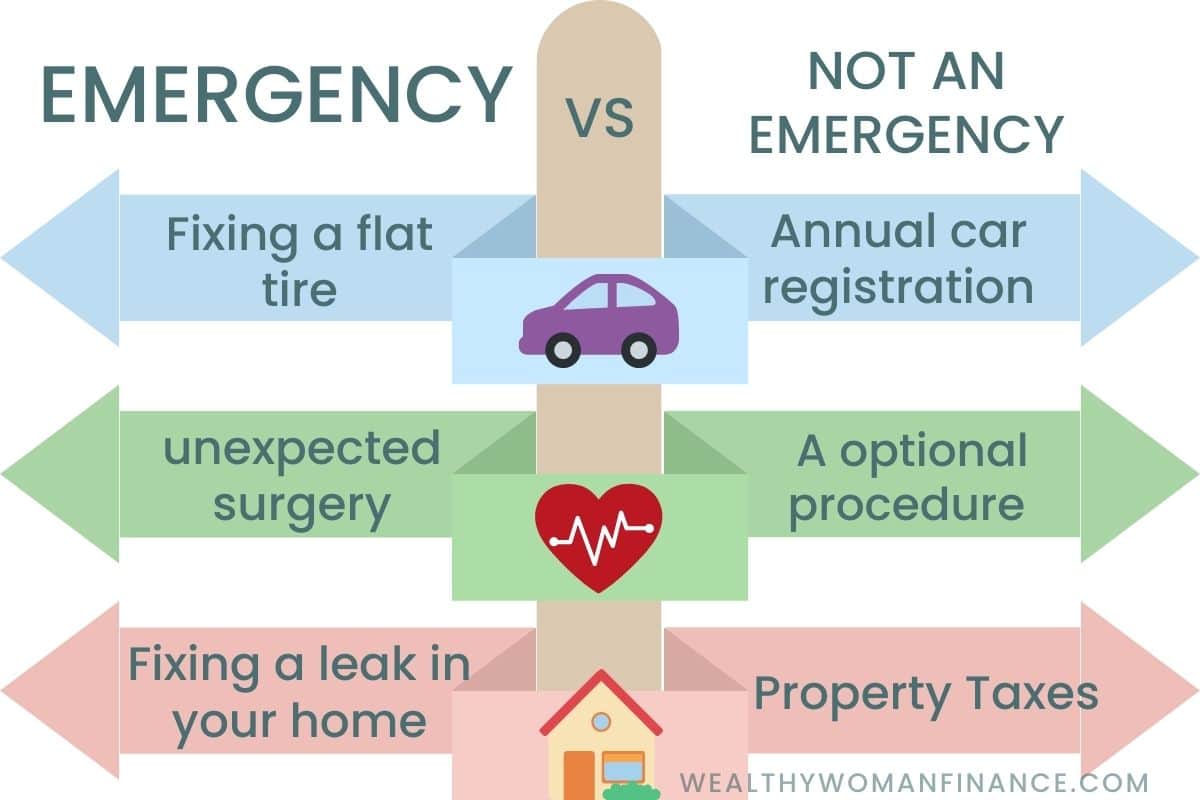

2. Build an Emergency Fund (AKA Your Shield)

First, it’s ok to start small. Aim to save at least $500 initially. Then gradually increase to cover 3-6 months of expenses. This cushion helps you manage during sudden financial hiccups, like job loss or emergency repairs.

Here’s how to get your emergency fund fully funded:

1. Start by calculating your monthly expenses.

2. Multiply your total monthly expenses by the number of months you want to cover. A clear goal gives you a tangible target to work toward.

For example, if your monthly expenses are $2,000, aim for an emergency fund of $6,000 to $12,000.

3. Set up an automatic transfer from your checking account to your emergency fund savings account on payday. This ensures that you save a portion of your income before you have a chance to spend it!

Clever Strategies for Saving Consistently

Next, the habit of saving a portion of each paycheck gives you financial security and peace of mind. Even if it’s small!

Here are several strategies to help you start saving:

1. Don’t forget the power of small purchases. Things like making coffee at home instead of buying it or reducing takeout meals add up quickly.

2. Put financial windfalls—like tax refunds or bonuses—directly into your emergency fund. This boosts your savings without impacting your regular budget.

3. Cancel Subscriptions: Review and eliminate unused or non-essential subscriptions and memberships.

4. Meal Prep: Plan and prepare meals at home to reduce dining out costs. See: My Rotating Meal Plan.

5. Avoid Lifestyle Inflation: Resist the urge to increase spending when your income rises.

Pro Tip: If impulsively buying things is a problem, remove temptation as much as possible. Take a different route to work or remove all shopping apps on your phone (only buy on your computer). Make impulse shopping as hard as you can. Then replace it with a less expensive hobby, like reading books from the library or building a side business.

3. Break the Debt Chains

Next, prioritize paying down debt! Interest can accumulate in the blink of an eye. It’s one of the number one reasons people never get ahead of their bills. They struggle to get ahead of their debt.

The Debt Snowball and Debt Avalanche methods are popular strategies to tackle debt.

The Debt Snowball method involves paying off your smallest debts first, regardless of interest rates. This can provide quick wins and motivational boosts, helping you stay committed.

- List your debts from smallest to largest.

- Make minimum payments on all debts except the smallest, which you target with any extra money.

On the other hand, the Debt Avalanche method focuses on paying off debts with the highest interest rates first. This approach saves money on interest in the long run but might take longer to see significant progress.

- List your debts from highest to lowest interest rate.

- Pay the minimum on all debts, directing any extra funds to the highest interest debt.

Use these free debt trackers to help you see progress!

Other Great Debt Options

These are a few other things you can do while tackling your debt.

Debt consolidation involves combining multiple debts into a single loan (generally personal loans or balance transfers). This can:

- simplify your repayment process, making it easier to manage

- possibly result in a lower interest rate (saving you lots over time)

Refinancing is another option where you obtain a new loan to pay off existing debts. It’s often at a lower interest rate. This can reduce your monthly payments and the total interest paid.

Make sure you understand the terms and fees associated with any new loan.

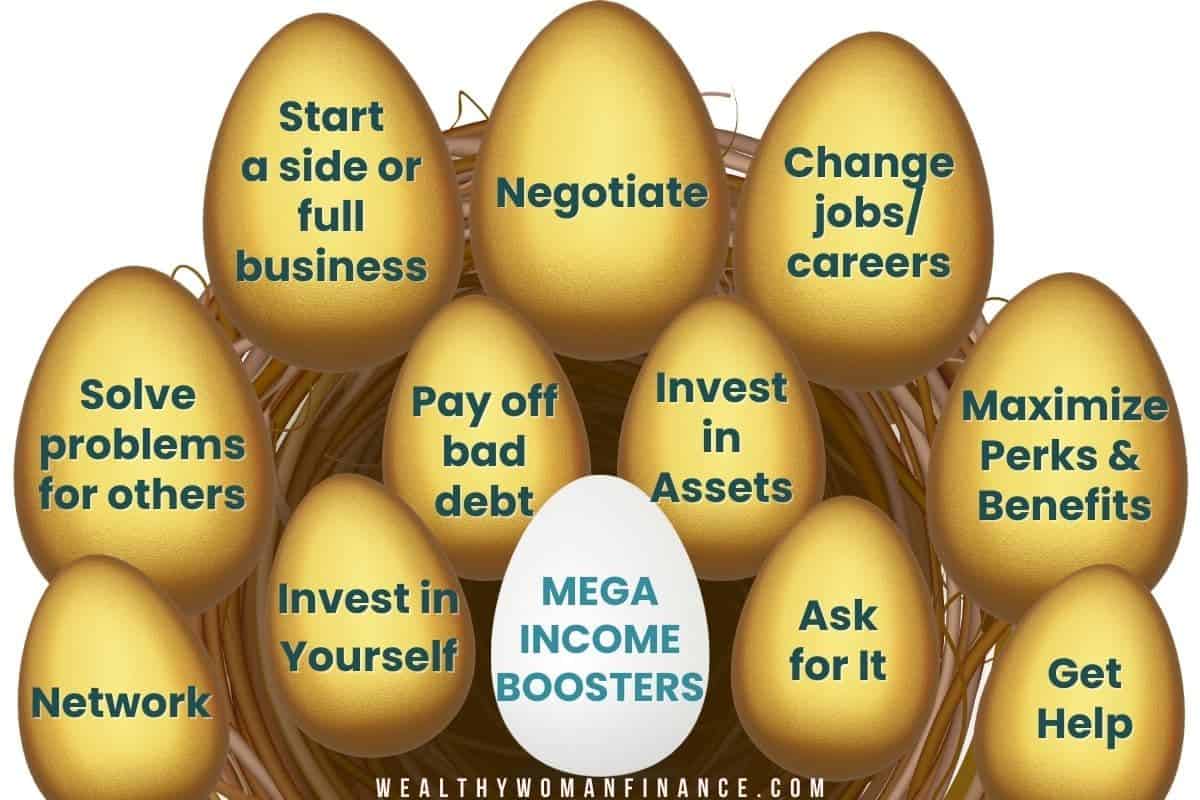

4. Increase Your Income ASAP

Pursue Career Advancements

Start by identifying opportunities for promotions or higher-paying positions. This often requires working on new skills through:

- certifications

- training programs

- or even higher education

Networking also plays a crucial role. Make connections with industry professionals through platforms like LinkedIn or by attending industry events. These relationships can open doors to new job opportunities and career growth.

Additionally, negotiate your salary during performance reviews. Know your worth! 10% more now means 10% more over the rest of your career! This is the difference in tens to hundreds of thousands of dollars over time.

“If you don’t value your time, neither will others. Stop giving away your time and talents. Value what you know and start charging for it.”

—Kim Garst, marketing strategist

Explore Opportunities Outside of Your Main Job

Diversify your income streams through side hustles and passive income to enhance your financial stability. Look into freelance opportunities that leverage your skills, such as writing, graphic design, or consulting.

I’ve hired people from both Upwork or Fiverr for digital freelance work.

Passive income is also a valuable strategy.

- Options include investing in stocks or real estate, where you can earn dividends or rental income.

- Consider creating digital products like e-books, online courses, or apps. These can generate sales long after the initial launch.

Related: How to Turn $1,000 into $100,000

5. Invest in Yourself

Investing in yourself is one of the most powerful ways to break out of the paycheck-to-paycheck cycle. As in #4, enhancing your qualifications can open doors to higher-paying job opportunities.

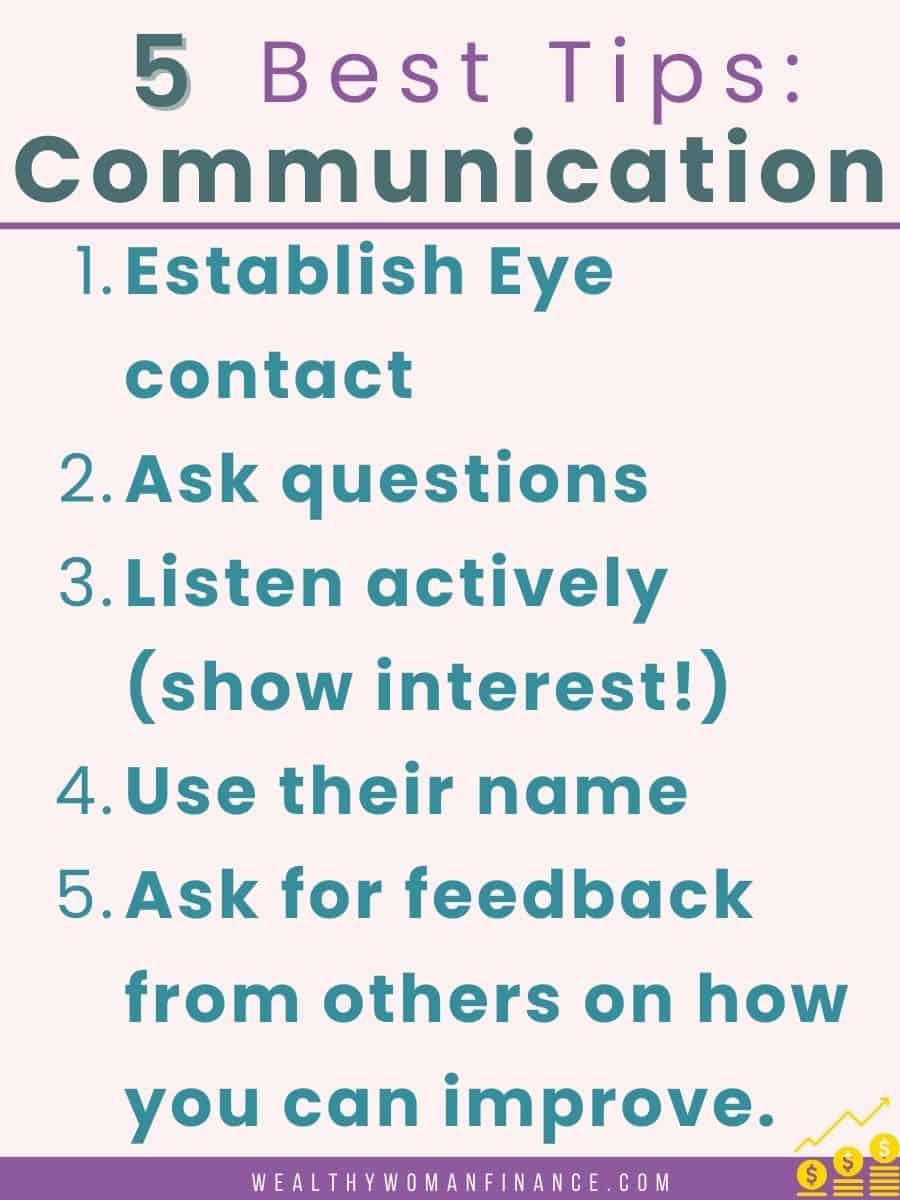

Also work on developing soft skills, such as communication and leadership. These are equally important and make you valuable and versatile.

Invest in Your Health and Wellbeing

Your health also directly impacts your ability to earn and save money.

- Regular exercise and a balanced diet improve productivity and reduce medical expenses. Incorporate activities like walking, yoga, or a simple workout routine.

- Practices like meditation and mindfulness reduce stress and improve focus. Ensure you manage stress effectively to avoid burnout.

- Routine check-ups and preventive care can catch potential health issues early, saving you from costly medical bills later.

- Prioritize sleep, as it significantly influences your overall well-being.

6. Start Investing Elsewhere Too

Once you’re on solid footing with an emergency fund, less debt, and a bit of savings, consider investing for your future.

Retirement Savings Plans

Starting a retirement savings plan early can have a significant impact on your financial health. One popular option offered by many employers is the 401(k).

Contributing to a 401(k) often includes employer matching, which is essentially FREE money towards your retirement.

If a 401(k) isn’t available, consider an Individual Retirement Account (IRA), which comes in two varieties: Traditional and Roth.

- Traditional IRAs offer tax deductions on contributions

- Roth IRAs provide tax-free withdrawals in retirement.

Evaluating each can help you maximize your retirement savings.

Consistent contributions are crucial. Even small, regular investments can grow substantially over time through the power of compound interest.

Pro Tip: Automatic transfers from your checking account to your retirement savings simplify the process and ensure you stay on track.

7. Seek Financial Advice

Finally, take the approach to finance that goes something like…

“Don’t let your learning lead to knowledge. Let your learning lead to action”

― Jim Rohn

Read books, attend workshops, and dig into credible articles to improve your financial literacy. You can also consult with a financial advisor for personalized guidance.

Then take the knowledge, and implement it into your money management as you learn.

Even if your progress is slow, as long as you’re moving in the right direction, you will get there. And with all 7 strategies in action, it might be much sooner than you believed!

Don’t forget to save this on Pinterest for later!

What’s Next?

Grab ongoing wealthy woman ideas in the newsletter. Make money-smart decisions your default, plus gain instant access to the free resource library.