Top 10 Money Rules to Live By for Financial Freedom

While the world of finance can seem complex and irrational, the wealthiest people (who make money but also sleep soundly) adhere to a simple set of money rules.

These money rules are the fundamentals. They are the foundation that keeps the rest of your financial house standing. So, get good at the basics! Once you do, you can tune out the noise the majority of people put up with.

Want to save this idea?

It’s not just about hoarding every penny. It’s about making sure that your money is working toward your goals. Whether it’s buying a home or saving for retirement, these top 10 money rules offer a balanced approach.

Rule #1: Live Below Your Means

Living below your means is the practice of spending less than you earn.

Bottom line: High-income folks go broke every day. And it’s not because they don’t make enough money. They don’t control their spending.

This practice allows you to build savings, reduce stress, and prepare for future financial challenges. Here’s how to make sure you do it:

Set a Budget

A budget acts as a financial compass. The popular 50/30/20 rule breaks down income into necessities, wants, and savings. Here’s how it might look for you:

- 50% on Needs: Rent, utilities, groceries.

- 30% on Wants: Dining out, entertainment, luxuries.

- 20% on Savings/Debt: Emergency fund, retirement, sinking funds, debt payments.

To stay on track, regularly review and adjust your budget.

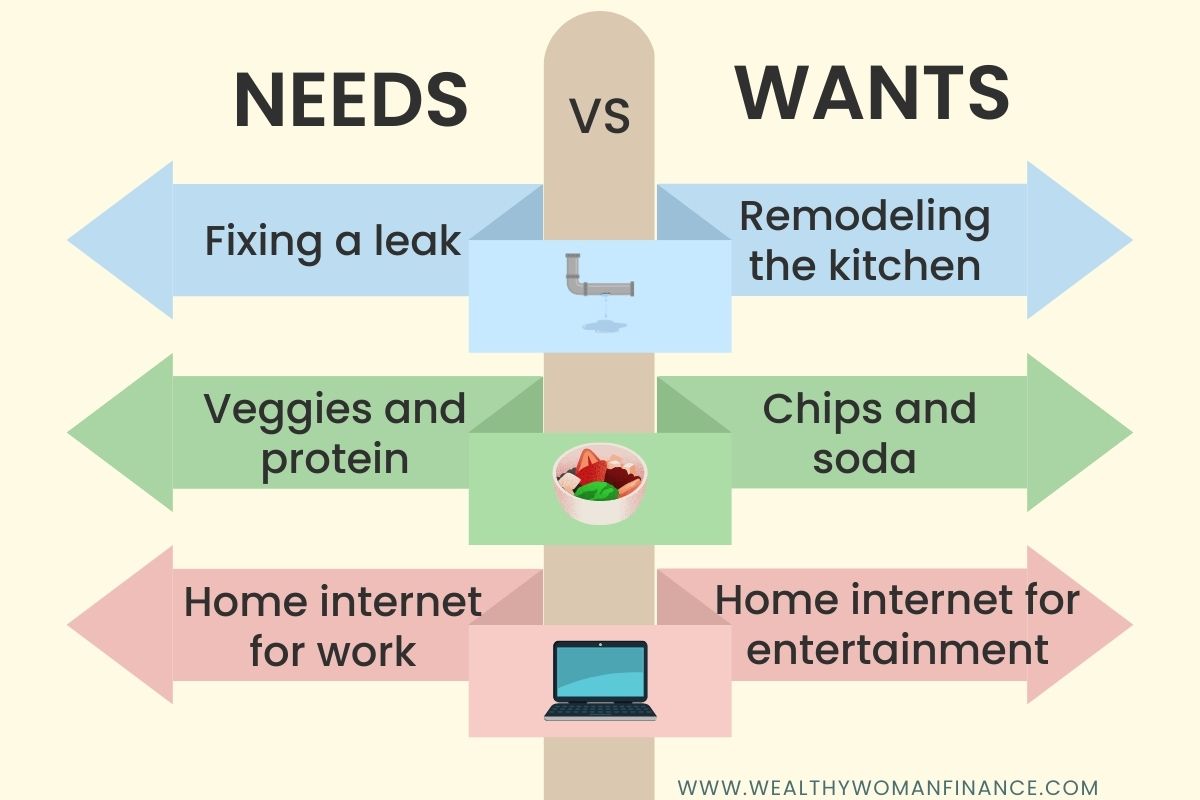

Understand Needs vs. Wants

Distinguishing between needs and wants is vital to your financial well-being. Otherwise, it’s too easy for the lines to blur.

- Needs are essentials required for survival and basic comfort, like shelter and food.

- Wants are items or experiences that enhance your life but are not necessary, such as the latest electronic gadget or a vacation.

By categorizing your spending, you make it easier to prioritize and identify areas to cut back.

Rule #2: Build an Emergency Fund

Think of your emergency fund as your superhero shield. It protects you from anything life might throw at you. Even those nasty sucker punches!

How much do you need?

You should have at least three to six months’ worth of living expenses. This money covers the necessities.

Grab an emergency fund challenge and use the calculator there to calculate your needs.

Strategies for Emergency Fund Saving

Make regular contributions. Set up an automated transfer to your fund. This keeps you consistent and helps you build the habit of saving. Without having to remember each time.

High-Interest Savings Account: Choose a high-yield savings account and you’ll make more money without any extra effort. Many of these exist with online banks.

This ensures your money isn’t idle but rather growing, albeit slowly, in the background.

Cut Expenses: Analyze your budget and find creative ways to save, like building a capsule wardrobe and having fun with friends on a budget.

Make Extra Income: Any additional income, whether it’s tax refunds, bonuses, or side gig earnings, goes directly into your emergency fund.

Rule #3: Eliminate and Avoid Debt

Managing finances wisely involves paying off debt and making choices that avoid accumulating debt that doesn’t serve you. These are crucial steps for financial stability.

Pay Off Existing Debt

Try the debt avalanche method, which focuses on repaying debts with the highest interest rates, then moving to those with lower rates. This saves you the most over time.

For example, credit card debts often have higher interest rates than other loans. By paying more than the minimum payment, you reduce the principal faster and decrease the total interest paid.

Avoid New Debt

Save in advance for big purchases, like a car and down payment on a home. This savings gives you massive advantage in the long-run, boosting you into millionaire status over time.

Saving for cars before buying them was one of the most influential factors for wealth in my own life. By knowing this early, I was able to invest while others were paying off this debt.

Related:

Rule #4: Invest Early and Often

Investing sets the foundation for financial growth.

Use Compound Interest to Your Advantage

Compound interest is the interest on interest. It’s the initial amount plus the interest your investment has generated in previous periods. When you invest early, the amount has more time to grow.

For instance, assuming an annual return of 7%, investing $1,000 now is equivalent to over $7,600 in 30 years, purely through compounding. (You didn’t add anything to it!)

Diversify Investments

To manage risk, diversify across various investment classes. By spreading out your investments, you reduce the impact of any one asset’s poor performance. A balanced mix might include stocks, bonds, and real estate.

For example, if the stock market declines, your bonds may buffer the loss.

Diversification is not just about picking different assets, but also choosing investments in different industries and geographic regions. Investing in yourself is another great way to use your money well while diversifying.

Rule #5: Protect Your Income

Managing your money well includes safeguarding your earnings. This requires the strategic use of insurance and legal measures to protect against loss of income.

Insurance Policies

Health, disability, and life insurance are essential coverages that protect you and your family from the financial hardships that can arise from illness, injury, or death.

- Health Insurance: Ensures that your are not financially burdened by medical expenses.

- Disability Insurance: Provides income if you are unable to work due to a disability.

- Life Insurance: Offers financial support to your beneficiaries in the event of your passing.

Legal Directives

Wills and living trusts are crucial tools as well. These legal documents ensure that your assets are distributed according to your wishes. Plus, they provide clear instructions should you become incapacitated.

- Will: Outlines your wishes regarding the distribution of your assets after death.

- Living Trust: Offers a way to manage your assets during your lifetime and distribute the remaining assets after your death.

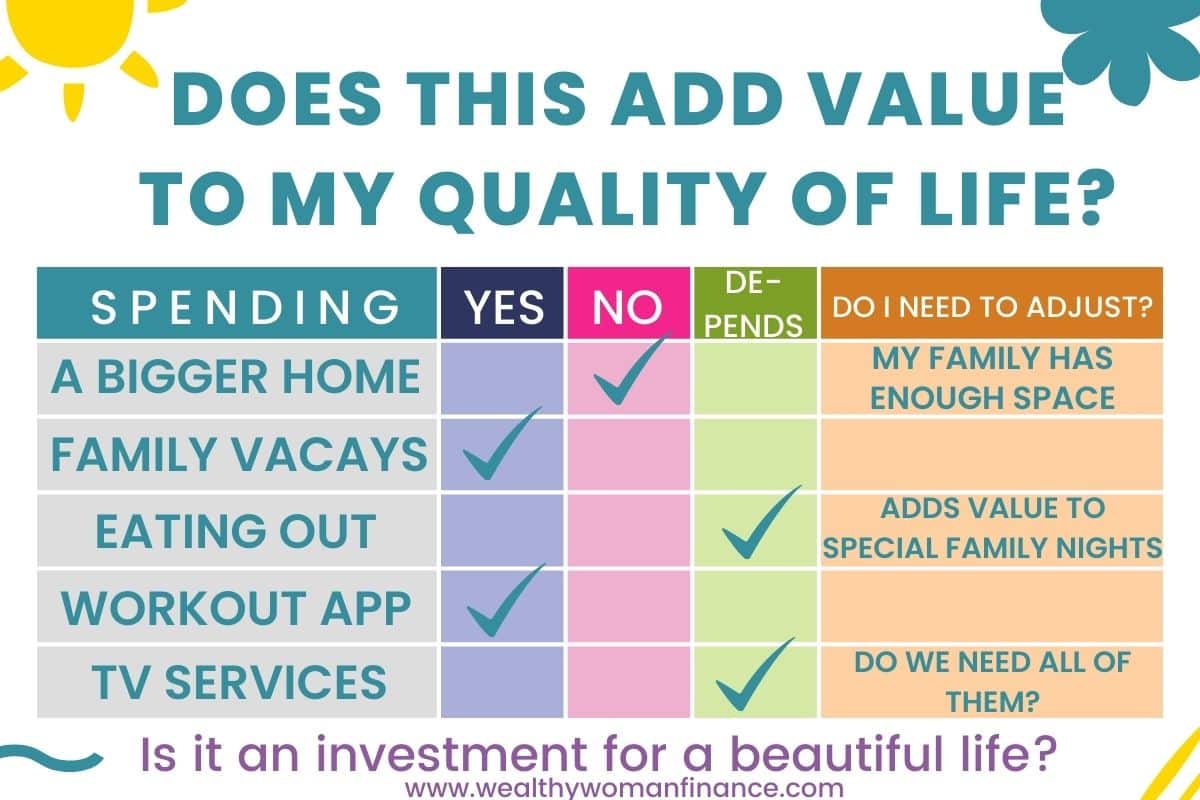

Rule #6: Spend Mindfully

Engaging in mindful spending is not merely about saving money. It’s about investing in what truly adds value to your life. It requires a shift from impulsive buying to an intentional approach.

One where every dollar spent reflects your money values and money goals.

Does it Make your Life Better?

Before you buy, ask yourself if what you are buying is going to make your life better. It’s a simple rule I follow, that I like to call the “quality of life lens.”

This subtle question ensures that your spending habits support your true priorities. Not just short-term whims. It’s a strategy that leads to significant savings, goal alignment, and drastically lower stress.

Rule #7: Increase Your Earnings

Increasing your income over time is crucial for financial success. Particularly for women, who get stuck earning less than men.

Career Advancement

One of the most effective ways to boost your earnings is through career advancement.

- Seek out certifications and professional development

- Network within your industry to open doors to higher-paying opportunities

- Take on projects that increase your visibility and demonstrate your skills.

- Ask for it! Often women are qualified. They just don’t push for what they deserve. Understand the value that you bring to the table!

Passive Income Streams

The average millionaire has 7 streams of income. In many cases, at least one of these is passive. There are many ways to achieve this.

- invest in high-yield savings accounts

- participate in the stock market

- Invest in rental properties

- Start a passive income side gig

These are just a few! By diversifying your income sources, you mitigate risk and maximize the potential for consistent earnings.

Rule #8: Plan for Retirement

Preparing for retirement is a cornerstone of sound money management. Focus on setting aside a portion of my income for the long haul.

Retirement Accounts

Do your best to maximize contributions to your retirement accounts annually. This can be through a 401k, self-employment SEP, and/or an IRA. Not sure on this? Ask your accountant or a financial advisor what your best options are and how much you can put in.

Make Long-Term Goals

Don’t just hope to save more. Instead, set clear, attainable long-term goals. This helps you break down your numbers to how much you need to save each year and month. Use tools like retirement calculators to estimate.

Rule #9: Give Generously

Giving is about supporting the communities and causes that matter. It also puts you in an abundance mindset – one where you don’t feel lacking.

Giving reflects your values. What kind of person do you want to be?

Charitable Contributions

It’s important to do research and select organizations that have a transparent track record. Not only is this an opportunity to help others, but these contributions can often be tax-deductible.

Community Support

Investing your time and resources, whether it’s sponsoring a youth sports team or a local food drive, will be fulfilling, provide networking opportunities, and strengthen the community in which you live.

Rule #10: Never Stop Learning

Finally, self-education is the cornerstone of every financial empire.

Financial Literacy

Prioritize financial literacy to make informed decisions with your money. This involves understanding concepts such as interest rates, investments, and the effect of inflation on savings. You can:

- read money books

- peruse Wealthywomanfinance.com

- sign up for the Wealthy Woman Newsletter

- take online courses

- attend workshops and more.

Everyone starts at the beginning. So, if you’re feeling intimated by the world of finance, know that each step in the journey matters. And the best way to build confidence is to make your learning a priority.

What’s Next?

Live by these 10 money rules and you’ll be on your way to millionaire (and maybe even billionaire) in no time. Because you can’t get there without them!

In fact, they are the exact rules I’ll be teaching to my own kids.

Next, join the Wealthy Woman community. It’s a growing number of women building wealth now!