Best Year End Financial Planning Checklist to Get Ahead

A financial planning end of year checklist can help you go from not knowing what to do to setting you up for massive success.

Don’t just plan for the next week or month. But make sure that your family has a financial future for the long term. 5 years from now, you’ll be so glad you did.

Pro Tip: Make your financial planning session enjoyable! Put on soft music, make it a restaurant date with your partner, or block off a peaceful afternoon to focus.

Want to save this idea?

The great thing about this free checklist is that it can be done any time of year! Use it to evaluate whenever you need to check where you are!

Financial Planning Checklist

These are things to do before the end of the year that organize, re-align, and clarify your financial future. They are not to be taken lightly!

1. Review Your Budget and Expenses

*Use a spreadsheet or budgeting app (I love Mint.com) to make this step easy.

Pull up your monthly expenses and evaluate your budget. Compare your actual spending to what you had initially planned to spend. Are you living below your means?

Look through each of your budget categories for signs of overspending and where you can cut back.

Pro Tip: Divide your spending into needs and wants to better understand your spending habits.

By identifying ways to save, you can get your budget back on track and be better prepared for the upcoming year.

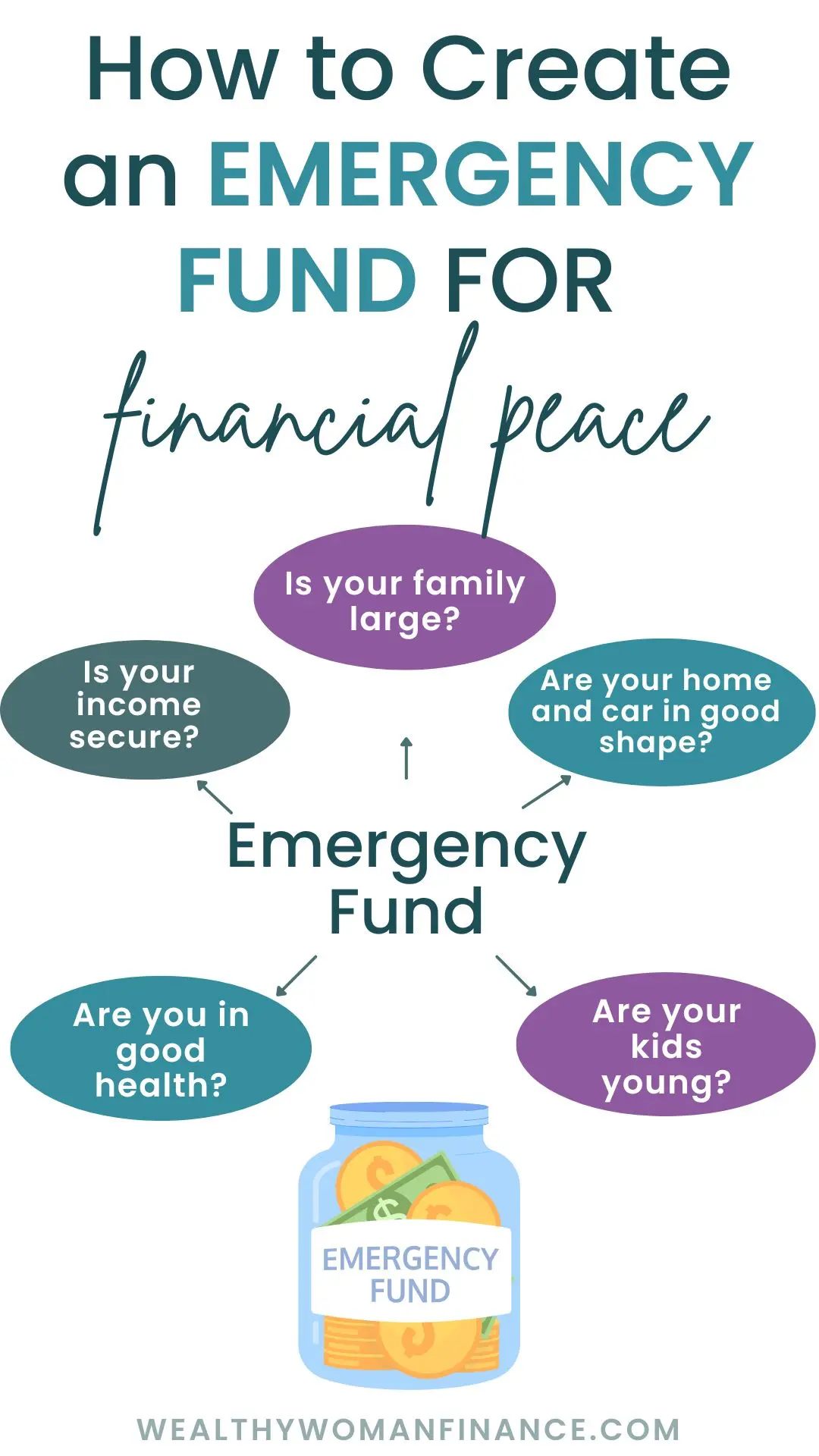

2. Check Your Emergency Fund

An emergency fund is a critical piece to your end of year financial planning checklist. Without one, you’ll be riddled with stress and debt when medical bills or car repairs happen. Instead, prepare ahead for life’s unexpected surprises!

Make sure you have at least three to six months of living expenses in a high-yield savings account or money market account. (liquid net worth)

To find your goal number, look at your monthly expenses, then multiply by 3, 4, 5, or 6 (months) to get your goal amount.

Next, look at your current emergency fund. Compare it to your calculated target. If it falls short, don’t worry, just take action!

- Try an emergency fund challenge to boost your savings

- Set up automatic transfers from your paycheck to a savings account

- Cut back on spending or increase your income.

By checking in on your fund, you can make any necessary adjustments needed before it’s too late.

3. Create & Review Financial Goals

Without knowing where you want to go, how will you ever get there? Not only do goals give you clear direction, but they also provide motivation when saving becomes tough.

1. To start, make a list of general financial objectives you want to achieve in three months, six months, 1 year, and/or 5 years. Some common ideas include:

- Building an emergency fund (#1 priority!)

- Paying down debt

- Increasing your credit score

- Saving for big purchases

2. Next, pick your top three, and make SMART goals for each one.

SMART stands for Specific, Measurable, Achievable, Relevant, and Time-bound.

For example, instead of saying you want to save more money, set a goal to save $5,000 by October 15th for a down payment on a car.

3. Now that you have your list of SMART financial goals, think about the actions you’ll need to take to achieve each one. Work on your financial plan for the next three months.

4. Keep track of your progress with a goal tracker. There are many on this site for specific goals you’re working towards:

- Vacation Savings Tracker

- Paying Off Car, Home, Student Loan, & Credit Card Debt

- Christmas Savings Tracker

You can also use a checklist or spreadsheet (like the one below) to track.

| Financial Goal | Start of Year Status | End of Year Status | Progress |

|---|---|---|---|

| Emergency Fund | $1,000 | $4,000 | ✔ |

| Pay off Credit Card Debt | $6,000 | $4,500 | ✔ |

| Retirement Fund | $20,000 | $25,000 | ✔ |

Tracking your progress can help you stay motivated and make adjustments to your plan. Celebrate your milestones as you get closer to your goals!

If you already have goals, evaluate how you did in the last year. Are you getting closer? Do you need to make adjustments? Are these goals clear enough and have action steps to achieve them?

4. Evaluate Your Insurance Needs

*May take researching different insurance options.

It’s crucial to evaluate your insurance needs at least once a year. Small changes in your coverage can put you in a better financial position and provide peace of mind.

Evaluate all coverages – including life, health, car, and property insurance. Ensure your coverage aligns with your current needs and update beneficiaries if necessary.

First ask yourself:

Have my circumstances changed over the past 12 months? (Births, change in income, disability, moving, death, paid off mortgage, etc.)

Then, look at if your coverages have changed or if other options exist that would be a better fit for you.

Pro Tip: It’s also a great time to make sure you’ve taken advantage of any incentives insurance offers.

5. Have a Clear Debt Management Plan

A solid debt repayment plan will ensure you make consistent progress, even if curveballs come your way.

*Difficulty depends on your financial situation.

There are two popular debt repayment strategies to use:

- Debt Snowball (A Popular Dave Ramsey Method): You repay the debt with the smallest balance first. Once that’s paid off, move on to the next smallest debt, and so on. This method gives you quick wins and motivates you to keep going.

Debt Snowball Example

| Debt Name | Balance | Interest Rate | Minimum Payment | Extra Payment |

|---|---|---|---|---|

| Credit Card | $500 | 6% | $25 | $75 |

| Student Loan | $2,000 | 5% | $100 | $0 |

| Car Loan | $3,000 | 7% | $75 | $0 |

- Debt Avalanche: You prioritize debts with the highest interest rates. This approach saves you the most money in interest payments.

Debt Avalanche Example

| Debt Name | Balance | Interest Rate | Minimum Payment | Extra Payment |

|---|---|---|---|---|

| Credit Card | $500 | 6% | $25 | $0 |

| Student Loan | $2,000 | 5% | $100 | $75 |

| Car Loan | $3,000 | 7% | $75 | $0 |

6. Check Retirement Contributions

At the end of the year, evaluate if you are saving enough in retirement, and if you can save more.

One of the easiest ways to optimize your retirement savings is by taking full advantage of your employer’s match. Many companies offer to match a certain percentage of your contributions to the company-sponsored 401(k) or similar plans.

Check your pay stub and retirement account, or talk to your HR department for more information about your employer’s matching program.

Consider IRA Contributions

In addition to your employer-sponsored retirement plan, you can also make contributions to an IRA. IRAs provide additional tax benefits for investing.

There are two main types to choose from: Traditional IRAs and Roth IRAs. What you can contribute for both depends on your income and whether you participate in an employer plan.

- Traditional IRA: The earnings in a traditional IRA grow tax-deferred. You only pay taxes when you withdraw funds in retirement.

- Roth IRA: Contributions to a Roth IRA are made with after-tax dollars, but qualified withdrawals in retirement are tax-free. Roth IRAs are also more flexible because there are no required minimum distributions during your lifetime.

7. Evaluate & Rebalance Your Investment Portfolio

Are your investments aligned with your goals, risk tolerance, and time horizon?

*Many online brokerages will run these numbers for you. But this step requires time.

When it comes to effective end of year financial planning, assessing and rebalancing your investment portfolio is key. This ensures that your investments are in line with your desired risk level, time horizon, and financial goals.

First, take a look at your current portfolio and compare it with your target asset allocation. If it’s off, it’s time to rebalance.

Rebalancing involves selling high-performing assets and using those proceeds to buy assets that have underperformed. It brings your portfolio back in line with your target allocation.

Remember to consult with financial professionals for personalized advice based on your unique financial situation.

8. utilize tax strategies to Keep More Money

*Depends on your financial situation.

Next, make sure your finances are tax-efficient. Using tax strategies helps reduce your tax liability and keeps more of your hard-earned money in your pocket.

Maximize Deductions and Credits

Are you taking full advantage of deductions and credits?

- Contribute to retirement accounts: Maximizing contributions to tax-advantaged retirement accounts reduces your taxable income.

- Charitable giving: If you’re planning on making charitable contributions, do so before the year ends.

- Medical expenses: If your out-of-pocket medical expenses exceed a certain percentage of your adjusted gross income, you can deduct these expenses from your taxable income.

- Flexible Spending Accounts (FSAs): Generally, you must use FSA money within the year. So, if you have an FSA, schedule eligible medical appointments or purchase eligible items before the end of the year.

Harvest Investment Losses

Selling investments at a loss to offset capital gains on other investments is an effective strategy to minimize the taxes you owe on your gains.

Consider making a tax appointment with your accountant to ensure you’re taking full advantage of the opportunities and following tax code in your state.

9. Update Your Estate Planning

*Difficulty level depends on how much updating needs to be done.

A crucial step in your end-of-year financial planning checklist is to update your estate plan. Ensure that your plan reflects your current situation and wishes.

Here are aspects to consider:

- Review your will: Major life events like marriage, divorce, death, or the birth of a child can signal that it’s time to update.

- Update beneficiaries.

- Update power of attorney and healthcare directive.

- Revisit trust arrangements.

- Evaluate your assets and liabilities. If these have changed considerably, you may need to list them out so that you distribute your wealth fairly and there’s no unwanted financial burden on anyone.

10. Create Systems for Progress

Finally, a step that’s critical for success but not often talked about is the system you use to keep your finances in tip-top shape. Your end of year financial planning checklist is the time to make sure your financial goals don’t get stranded at the starting line.

A clear system ensures that you’ll keep making progress, even on your hardest days!

Answer these questions to develop clear processes around your most important financial priorities:

- Where do your bills go before they’re paid? After?

- When do you check your budget and spending? Do you have larger financial check-ins throughout the year? Is this alone or with your partner?

- Do you have a spreadsheet or software to track your spending, saving, and investing?

- Do you have automatic deposits set up for savings, investing, and debt repayment? Do they need to be changed?

- What gets in the way of your financial success? Can you remove this obstacle or create a system around it?

Free Financial Planning Checklist

Related:

What’s Next?

Next, save more money by making it fun! Gain inspiration every Thursday and instant access to the resource library full of money games and challenges.