12 Free Printable Budget Templates To Help You Save Big

If you’re feeling stuck with your money or tired of the rat race, it’s time to take control.

These free budget templates give you amazing options to start a new journey of better money management.

Every single budget system offers:

- Consistent savings

- Accountability. You’ll know what you can afford, and have a guide to use your money for your greater good.

- A way to measure. The numbers don’t lie! And you’re going to know immediately if your lifestyle is out of whack. If it is, just make adjustments to get back on track.

But first, you’ll be the most successful if you keep an open mind to changing the way you handle your finances.

Want to save this idea?

Understand That Everything Changes

In a quiet village, a wise Zen master sat before a group of eager young monks, sharing profound lessons about the meaning of life.

For hours, the master spoke while the students listened with unwavering focus. As the day drew to a close, one hesitant monk raised his hand and said, “Master, I must admit, I don’t fully grasp the depth of Zen—it feels so complex.

Can you share one simple truth we can hold on to?”

The master smiled gently and replied, “Everything changes.”

Starting a new budget (or any budget at all) is a process.

Change, after all, is never easy.

But if you accept it as a simple truth, the journey becomes one of discovery instead of restraint.

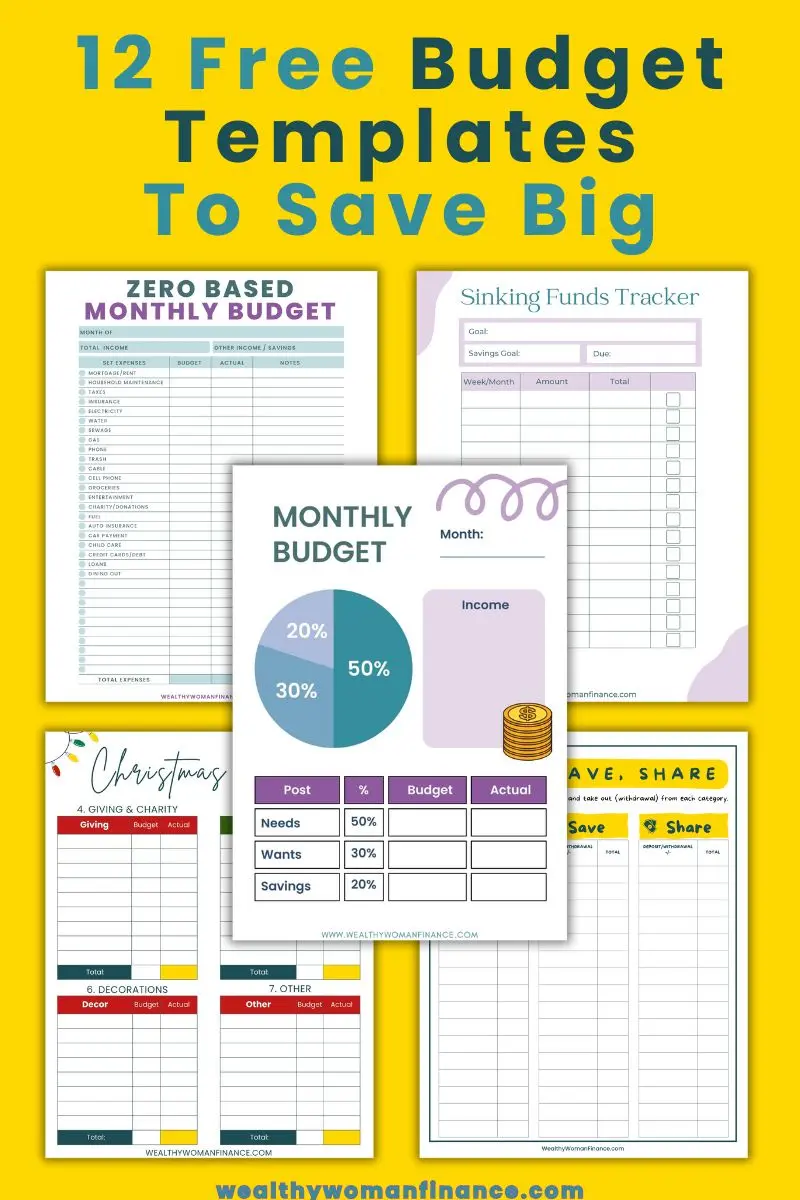

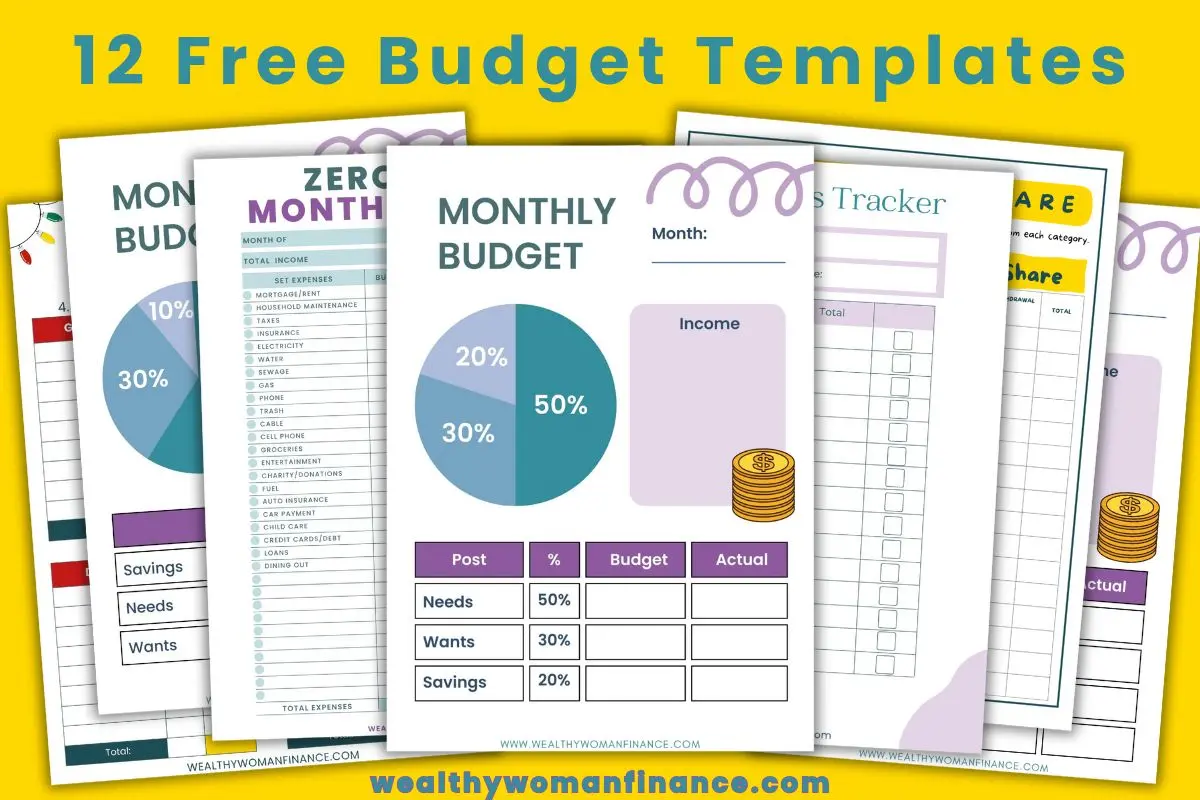

12 Budget Templates To Print for Free

So, which of these free budget templates will you use to take your discovery and learning to a new level? It’s time to find out!

Below, you’ll learn what each budget is, plus the pros and cons of each one.

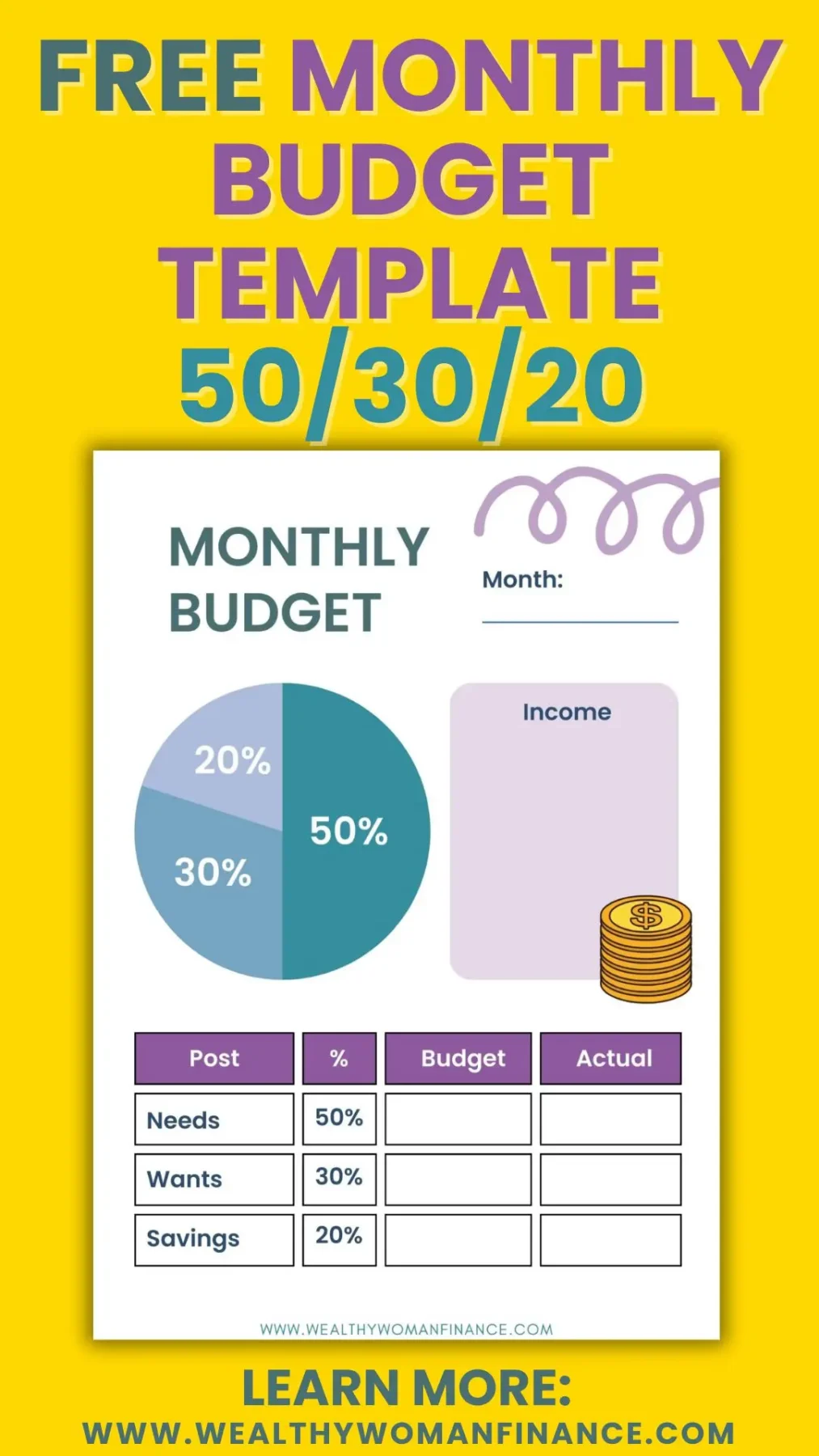

1. The 50 30 20 Budget

First, this is the simplest budgeting rule. It allocates 50% of your after-tax income to needs, 30% to wants, and 20% to savings or debt repayment.

Use the calculator on the post to see what your numbers would be.

See the 50 30 20 Budget Rule >>

| Pros | Cons |

| – It’s easy to follow, flexible, and encourages savings – perfect for beginners. – You have flexibility between your needs and wants in this budget. – You’ll now be saving 20% each and every month. | – It may not work for people with high debt or in high-cost-of-living areas because needs might be higher. – There aren’t specific sections for giving or debt, so you’d need to lump them into savings. |

2. Zero Based Budgeting Template

Zero based budgeting is just like it sounds! Instead of trimming your expenses (like with most traditional budgets), you rebuild your budget from the ground up. Then, when you finish creating your budget, your expenses and savings equal your income.

Think of zero based budgeting as that of building a new invention. Sometimes, you need to stop trying to improve on what someone else has built. Instead, start from scratch to reset and innovate.

Use the calculator on the post to see what your numbers would be.

| Pros | Cons |

| – This budget is highly detailed. So, it ensures that no money is wasted. – It targets new and old expenses equally. You are looking at the big picture and taking a deeper approach. – You can create a new budget every month to fit the exact seasonal expenses you need. (How flexible!) | – It is more time-consuming and requires detailed tracking. If you have a great handle on your finances, this may be more than you need. – It can reward short-term thinking. Self investments like learning aren’t always as urgent, but they are equally (if not more) important long term. Keep this in mind! |

3. Reverse Budgeting Template

The unique reverse budgeting system focuses on savings first by setting a savings goal and allocating the remaining money for expenses.

Use the calculator on the post to see what your numbers would be.

| Pros | Cons |

| – This budget encourages aggressive savings and prioritizes financial goals. – It’s easy to automate. Which means that you will follow through. – It’s low maintenance. Once it’s set up, it’s very hands-off. – It naturally reduces impulsive purchases | – This budget can be challenging for those with tight finances, lots of debt, or unpredictable expenses. – It’s important to make sure you don’t squeeze yourself too hard. This could lead to overspending, which gets you in trouble on this budget. |

4. The 60 20 20 Budget Rule

With the 60/20/20 budget, you’ll start with your monthly after-tax income. Then, divide the money into 60% for needs, 20% for savings, and 20% for wants.

Use the calculator on the post to see what your numbers would be.

| Pros | Cons |

| – This budget is ideal for those with higher fixed expenses or needs. – It’s great if you’re struggling under a pile of bills, or you’re ready to get ahead financially. – You’ll now be saving 20% every month. | – This budget leaves less room for your “wants” compared to other percentage based budgets. – There’s no section for giving and you need to lump debt with the savings category. |

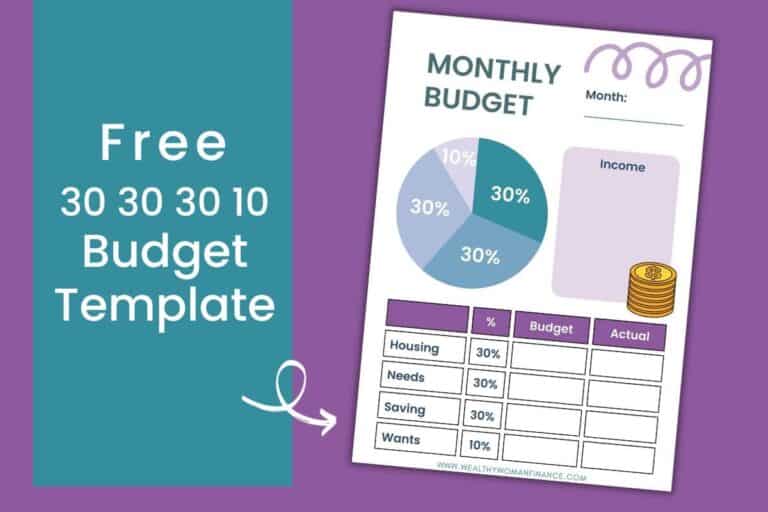

5. 30 30 30 10 Budget Template

With the 30-30-30-10 budget, you’ll start with your monthly after-tax income.

Then, divide the money into 30% for housing, 30% for needs, 30% for savings or debt, and 10% for wants.

Use the calculator on the post to see what your numbers would be.

| Pros | Cons |

| – This budget looks at housing as a separate piece of your budget. – Limiting wants in your budget accelerates progress. – You’ll now be saving 30% each month, which is a little more than some other budgets. Over time, compound interest of this extra savings will work wonders for you. | – If you live in a place like Los Angeles, fitting your housing into 30% will be difficult. In this case, it’s smart to put housing and needs together at 60% for more flexibility. – If you are used to spending a lot on your “wants,” you may want a different budget. – There’s no section for giving and you need to lump debt with the savings. |

6. Biweekly Budget Template

This is a budgeting method for those paid biweekly. It focuses on allocating income every two weeks rather than monthly.

| Pros | Cons |

| – This budget matches your pay schedule, so it helps avoid overspending between paychecks. | – It can be tricky to align with monthly expenses like rent or utilities. |

7. Christmas Budget Template

The Christmas budget template is a seasonal budget designed to plan and track holiday spending, including gifts, decorations, and meals.

| Pros | Cons |

| – This seasonal budget prevents overspending during the holidays. It helps you keep this high-cost time of year in check, so it doesn’t blow up your overall budget. | – It requires advanced planning. It’s best for planning out in October or November, before the craziness starts. |

8. 60 30 10 Budget Template

With the 60 30 10 rule, you’ll start with your monthly after-tax income (your take-home pay). Then, divide the money into 60% for savings, 30% for needs, and 10% for wants.

Use the calculator on the post to see what your numbers would be.

| Pros | Cons |

| – Putting 60% towards your financial future will shave YEARS off of your debts and the wait for financial freedom. You’re not dreaming about it. You’re doing it. And this lets the power of compound interest multiply. Once it starts adding up, you’ll be astonished at how quickly it grows. | – This is aggressive! And that means it’s not easy. It may not work for people in high cost of living areas or if you have higher needs. – There’s no section for giving and you need to lump debt with the savings. |

9. Sinking Funds Tracker

The sinking fund tracker is a budgeting tool to save ahead for specific future expenses (e.g., vacations, car repairs, kids activities). It works within your overall monthly budget.

Use the calculator on the post to see what your numbers would be.

| Pros | Cons |

| – Sinking funds are a great way to save money for things you know you will need to spend on in the future. And like everything, the best way to stay consistent is to keep track. – These funds also help you avoids nasty financial surprises. | – Building your sinking funds requires discipline to stay consistent. |

10. Needs Vs Wants Template

The needs vs wants tracker is a budgeting tool to differentiate between your essential expenses (needs) and discretionary ones (wants).

| Pros | Cons |

| – It can be easy to rationalize a want as a need. This tracker helps you take a deeper look into the stories you tell yourself. – It also helps prioritize your spending and eliminate expenses altogether. | – Some decisions are subjective, which can make categorizing items challenging. |

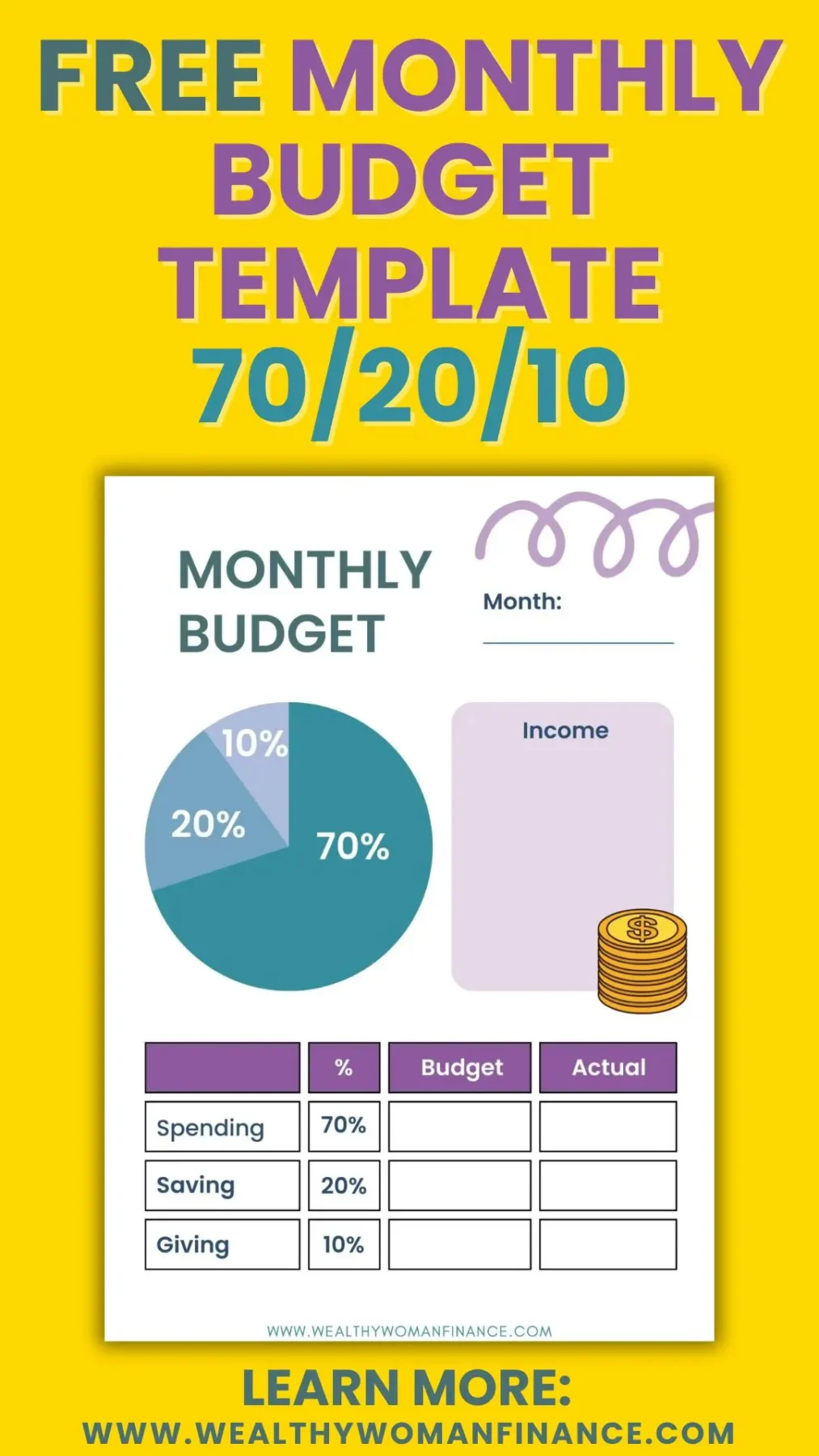

11. 70 20 10 Budget Template

With the 70/20/10 budget, you’ll start with your monthly after-tax income. Then, divide the money into 70% for needs and wants, 20% for savings, and 10% for debt repayment or donations.

| Pros | Cons |

| – This budget accommodates higher living expenses. – It’s flexible. Your wants and needs have more room to shift. – It’s amazing for anyone who wants to prioritize their debts or include giving in the budget. – You’ll now be saving 20% each and every month. | – Because your wants and needs are lumped together, it can be easy to give in to more “wants” that you don’t really need. – If 70% isn’t enough for needs and wants, try a less aggressive budget. |

12. Budget Template for Kids

Teach kids money management with a simple system: label three jars or envelopes as Spend, Save, and Share.

Then, use the free printable to track it. Keep it simple!

| Pros | Cons |

| – This budget builds financial literacy and healthy money habits early on. Way to set your kids up for life! | – It requires parental involvement and some form of consistency. – A printable can be hard for younger kids to visualize. For them, try jars or bowls with the money inside. |

Bonus: Baby, Car, & House Fund Trackers

These are visual trackers to monitor progress toward big life savings goals.

Check out the:

| Pros | Cons |

| – Trackers are motivating! They give a sense of progress and accountability to keep moving forward. – These trackers keep your large goals manageable by tracking baby steps. | – Goal trackers focus on specific areas, so they don’t always take into account your general budget. (You’ll need monthly budgets for that.) |

What’s Next?

Choose a free budget template and get started!

Next, keep the momentum going. Become a part of the Wealthy Woman community and receive my best tips for wealth-building. Begin now!

Don’t forget to save this post to Pinterest for later!