Master Your Money With the 60 20 20 Rule Budget + Free Worksheet

Whether you’re learning to budget or looking for an easy way to balance spending and saving, the 60 20 20 rule budget is a great option!

Now, this budget plan is great for beginners or advanced budgeters alike. There’s plenty of flexibility and it is particularly great if you have a family or live in a high-cost area where your needs may be higher.

Want to save this idea?

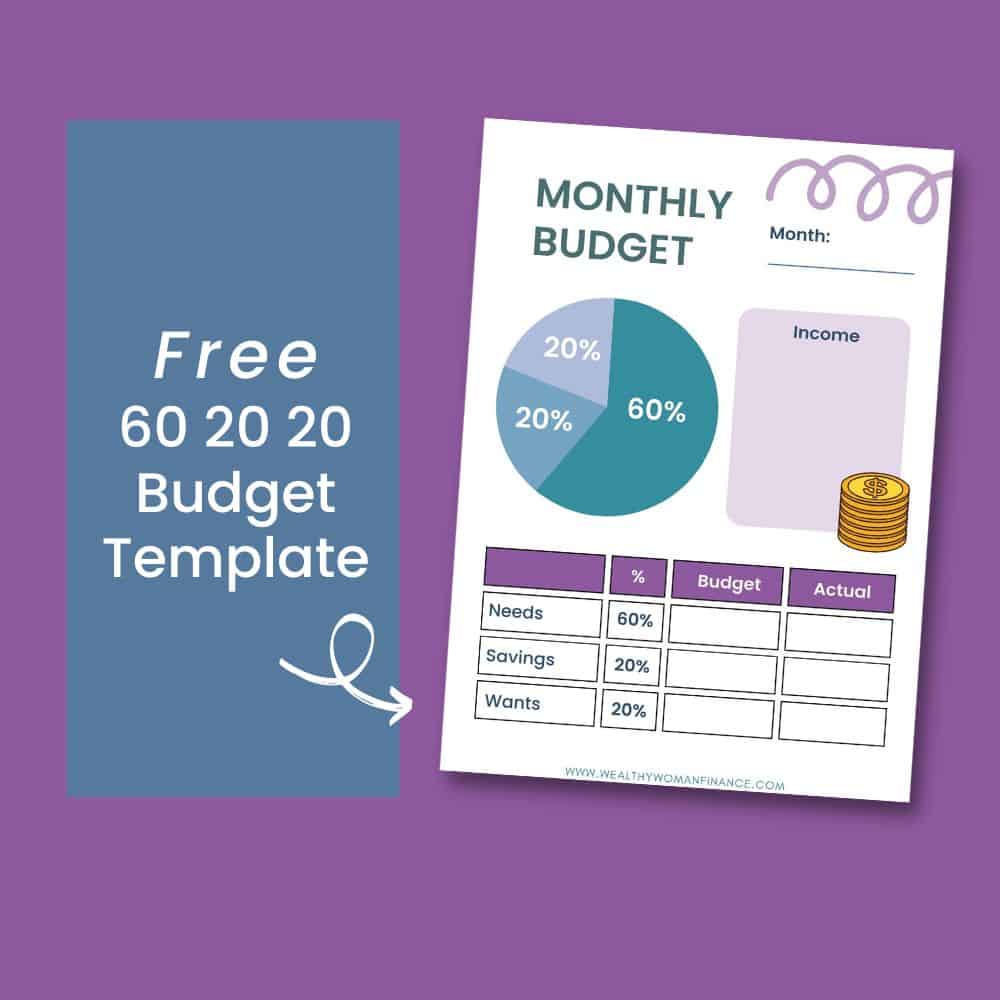

What’s The 60 20 20 Financial Budget?

With the 60/20/20 budget, you’ll start with your monthly after-tax income. Then, divide the money into 60% for needs, 20% for savings, and 20% for wants. With the 60-20-20 rule, you’ll be seeing exactly where your money goes, and if you’re overextending in certain areas.

What Are The Categories For The 60 20 20 Rule?

Now, let’s explore which subcategories fit under our “needs,” “wants,” and savings.”

- 60% on necessary expenses: Things like home, car, basic groceries, insurance, utilities, and childcare.

- 20% on savings: Things like emergency savings, retirement, college savings, and your bright beautiful future. (This also includes paying off debts if you have them)

- 20% on wants: Things like entertainment, cool stuff, eating out, and streaming services.

Here’s a bit more on each, so that you’re clear on what portions of your income go where…

60% Spending On Needs & Monthly Living Expenses

In this budget, your “needs” should include the things that are essential to your everyday life. Here’s a quick example of what your spending category could look like on this budget plan:

- Household Expenses (Mortgage, insurance, utilities, supplies, etc.) 25%

- Car Repairs, Maintenance, Insurance 10%

- Health Insurance/Healthcare 10%

- Food 10%

- Extra Necessary Kid & Pet Expenses 5%

Related: Needs Vs Wants Examples & Template

20 % Savings (60 20 20 Budget Rule)

Just like with your expenses above, you can divide out your savings however you want. Put it entirely into one account or split it up like below:

- Retirement 10%

- Saving for a Future Vacation 5%

- Paying off Your Car 5%

However you do it, consider all of the following excellent places to put your savings. (But remember, when investing your money there is always an element of risk):

Into Paying Off Debts

First and foremost, if you have nagging debts, you’ll want to take care of them first. With a 20% savings rate, you should be able to knock these out much quicker.

Create An Emergency Account

Next, build an emergency savings account. Not only will this keep you out of future debt when times get tight, but you’ll also breathe easier during a job loss, health emergency, or if you unexpectedly find water in your basement.

Speaking of a basement, think of an emergency fund as the foundation of your home. It’s what builds the rest of your house up. It’s the foundation that keeps your financial house from crumbling AT ALL TIMES.

<< Keep 3-12 months of monthly expenses in cash in a savings account >>

Save Money Into Sinking Funds

After your emergency fund is established, start saving for things you know you’ll need in the future. By having the cash ready, you’ll be able to enjoy milestones and look for great deals without money stress.

Here are great examples:

- Are you going to have a baby? Create a baby fund.

- Are you going to get married? Save up for that wedding!

- Will you need to replace your car? Create a fund to save for your new car.

- Kids activities get expensive. And vary by month. Start a kid activity fund to cover what you need all year long.

Related: Free Sinking Fund Tracker & Calculator

Put Money Into An HSA

Next, if you have an HSA available, use it! It’s like a medical emergency fund and it is tax-free as long as you use it for qualified medical expenses.

Put Money Into Retirement 401k, Roth, IRA

Next, if your company offers a retirement account match TAKE ADVANTAGE. That’s free money you’ll get to use later. And when you can, add even more money to your 401ks, and IRA accounts. These all have tax benefits that make them the smartest place to start out (and continue) investing.

Put Money Into College Funds

Do you have children you’d like to help with college someday?

Check out a low-fee 529. These are great because your money will not be taxed when you withdraw for educational expenses and some states offer other tax benefits (source). Or start your own custodial account that your kids can take over when they turn 18.

Invest: Stocks & Real Estate

Once you’ve covered the basic savings and investing options with tax benefits, explore other ways to invest your 20% savings. You can get started in real estate, invest in passive income stream opportunities, or buy stocks.

60 20 20 Budget Examples

Now, let’s look directly at a few 60 20 20 rule budget examples:

Let’s say you’re Jessica and you bring home $3,000 a month (after taxes). You’re single and living in an urban high cost of living area.

Your budget could look something like this:

- $1800 into things you need. Probably an expensive apartment, but also food, healthcare, and public transportation.

- $600 into savings for your emergency fund, retirement, or paying off your credit card debt.

- $600 into going out with friends on the weekend.

Now, let’s say your name is Natasha. You are married and living in a low-cost of living area. Between you and your spouse, you bring home $5,000, but this money stretches to take care of a family of five.

Your 60 20 20 budget example may look like this:

- $3000 into things you need. This pays your mortgage, supports your 2 car lifestyle, and covers other basic household food, supplies, and medical needs.

- $1000 into your savings. You’re splitting this between retirement accounts, your HSA, and college savings for the kids.

- $1000 into your streaming services, Friday night pizza, and kids activities.

As these examples show, everyone is different! You will have different budget categories and income levels. Play with the numbers to see what works for you.

60 20 20 Budget Rule Plan

Now, here’s a step-by-step guide for building a 60 20 20 budget:

1. Find your monthly after-tax income. If your paycheck lists your yearly rate, divide this number by 12 to determine your monthly amount. If not, add up your paychecks from the last year.

For example, if you get paid every other week, multiply your paycheck by 26 to find your yearly income. Then, divide by 12 to get your monthly average.

2. Divide out your monthly number by 60/20/20. Try the 60 20 20 budget calculator below to help you:

Monthly Total x .6 = Needs. Monthly Total x .2 = Savings. Monthly Total x .2 = Wants

3. Determine your essential needs first. What are the absolutes in your budget? Can you trim them up to make them easier on the budget?

4. Figure out what you’re saving for. Do you need to cover emergencies and sinking funds first? Set up an automatic transfer to put your money into savings every month.

5. Next, write out your wants. This is the category you have the most leeway with. Write the most important ones first.

6. Tweak and adjust as you go.

What Are The Benefits Of A 60 20 20 Budget?

Using the 60 20 20 budgeting money rule comes with incredible benefits. Here are just a few:

It Gives You Flexibility

You have a lot of flexibility between your needs and wants in this budget. If your needs are higher, make your wants lower. If your needs are lower, you have more money to use for your wants.

It Helps You See Where Your Money Is Going

For many, the real trick of budgeting is keeping track of the in and out flow of your money. With the 60-20-20 budgeting method, you’ll have a guide.

The 60 20 20 Budget Rule Helps You Save Every Month

This is a great budget if you’re struggling under a pile of bills, or you’re ready to get ahead financially. The BEST benefit is that you’ll now be saving 20% each and every month. This lets the power of compound interest work for you!

It Helps You See Missteps

The numbers don’t lie! And you’re going to know immediately if your lifestyle is out of whack. If it is, no worries. Just make the necessary adjustments to get it back in balance.

Grab The Free 60 20 20 Budget Template

A worksheet makes things easy! So snag yours now!

Grab more great free printables:

Which Budget Rule is Best?

While this article covers the 60 20 20, there are many different budget plans. The “best” one is the one that works for you! Consider your other options here:

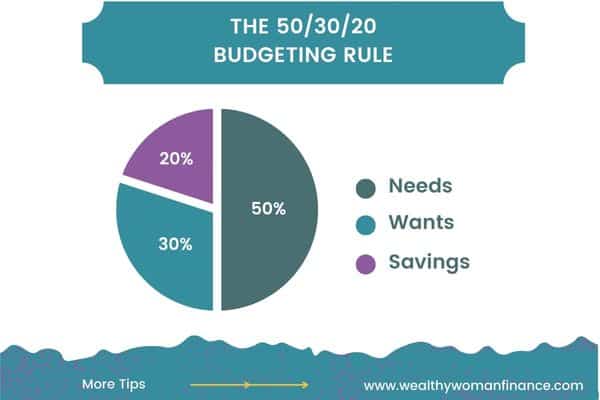

The 50 30 20 Rule (50% Needs, 30% Wants, 20% Savings)

Advantages of the 50 30 20: This method is the most popular budgeting rule. It allows for more spending on your wants, which works nicely if you have fewer needs.

Disadvantages of the 50 30 20: If you have more “needs” you might struggle to fit that into only 50% of your budget.

See a 50 30 20 budgeting template here >>

The 60 30 10 Rule (60% Savings, 30% Needs, 10% Wants)

Advantages of the 60 30 10: This method flips everything and has you saving 60%. It’s for the ambitious and it’s no joke! If you split up your savings into debt repayment and giving, you’d be able to do a lot with your money.

Disadvantages of the 60 30 10: Saving that much money is a big commitment. If you’re a beginner, or you just need to start with something steady and consistent, go with the 60 20 20 rule instead.

See more on the 60 30 10 rule for budgeting here >>

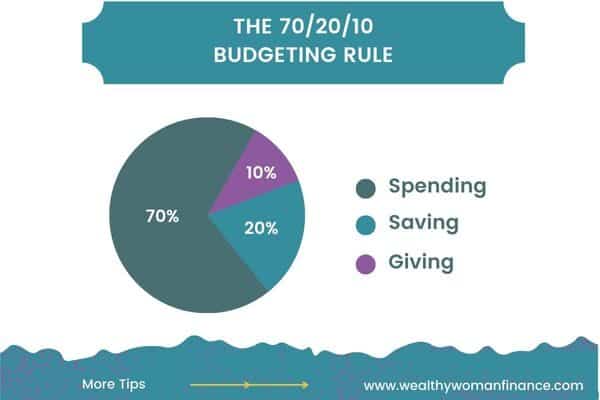

The 70 20 10 Rule (70% Needs & Wants, 20% Savings, 10% Donation/Debt)

Advantages of the 70 20 10 Rule: This rule puts needs and wants together, which makes it very flexible. It also has a specific allocation for donations or debts, which is unique from other plans.

Disadvantages of the 70 20 10 Rule: Using 30% for savings or debt can be a lot if you’re already struggling to make ends meet. Consider the 60 20 20 if you’re looking to ease your way into saving more.

See more on the 70 20 10 Budget Rule here >>

Common Q & As For The 60 20 20 Budget Rule

How Do You Do This Budget When Money is Tight?

Now, if your budget is already tight, you may need to get creative with bringing in more money.

- Consider starting a side hustle through a part-time job or flipping items on the side.

- Or try a free savings challenge printable to give you a jumpstart.

- And don’t miss these creative ways to save money (that you probably haven’t heard of)

Does The 60 20 20 Rule Include 401K?

In this budgeting rule, your 401k would be included under the 20% savings category. Your HSA will be under this too.

What Percent Of Income Should Go To Expenses?

When using the 60 20 20 budget a total of 80% of your budget will go towards your expenses.

How Do I Stay Motivated On The 60 20 20 Rule Budget?

Motivation comes and goes, but there are a few things we can do to keep the fire burning!

1. Create a money vision board with your financial goals and dreams.

2. Make smart financial goals that are specific and doable. These will also remind you what you’re fighting for.

3. Fill out a commitment card pledge. A little accountability will help you when your motivation wanes.

4. Motivate yourself with success and money affirmations, debt free living quotes, or other inspirational tools to keep you moving forward.